New

2 Spectacular Artificial Intelligence (ai) Stocks Primed To Beat The S&p 500 In 2025

The S&P 500 (SNPINDEX: ^GSPC) is up 28% this year, which is almost triple its average annual gain going back to 1957. It follows an incredibly strong year in 2023, when the index jumped 26%.

Those gains have driven the S&P to a relatively expensive valuation. It trades at a price-to-earnings (P/E) ratio of 27.8, which is a big premium to its long-term average of 18.1. That makes it very challenging to find value in this market.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

Technology stocks are leading the S&P higher at the moment, but those operating in the artificial intelligence (AI) space are generating particularly strong gains. That trend is likely to continue in 2025 as some of the world's largest tech companies spend record amounts of money to build AI infrastructure.

While AI stocks are some of the most expensive in the entire market right now, a couple of them still have the potential to beat the S&P 500 in 2025.

Image source: Getty Images.

There is still some value in big tech

Last year, a Wall Street analyst used the term "Magnificent Seven" to describe a group of large-cap technology stocks that were leading the market higher. The group includes Nvidia, Microsoft, Apple, Amazon, Tesla, Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL), and Meta Platforms (NASDAQ: META).

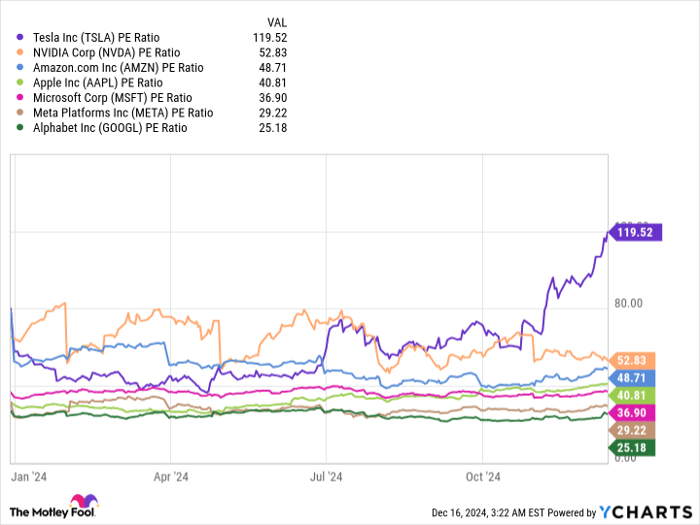

Each one of them is involved in the AI race in some capacity. However, in terms of value, Alphabet and Meta Platforms stand out because of their relatively cheap P/E ratios:

Here's why both Alphabet and Meta have the potential to beat the S&P 500 in 2025.

The case for Alphabet

Alphabet is the parent company of Google, YouTube, self-driving car company Waymo, and more. The conglomerate built its own family of large language models (LLMs) called Gemini, which sit at the foundation of an AI chatbot by the same name. But the models also power several new AI features within Google Search.

Most of Alphabet's revenue comes from the advertising dollars generated by Google Search. It's the world's largest internet search engine with a market share of 90%, but its dominance is under threat from third-party AI chatbots like OpenAI's ChatGPT, which are changing the way people access information online.

The Gemini chatbot is one way Alphabet is tackling those threats, but the company understands it also needs to change the user experience on Google Search. It launched AI Overviews earlier this year, which are AI-generated responses that appear at the top of traditional Google Search results. Overviews can include text, images, and links to third-party websites in order to give users faster access to information. The feature is rolling out to 100 countries right now, where it will serve 1 billion users per month.

Links within Overviews receive more clicks than the same links in traditional search results, so the feature could become a significant revenue driver for Alphabet. Monetization is likely to be a point of focus in 2025 because investors are seeking a payoff for the tens of billions of dollars companies like Alphabet have spent to develop AI so far.

There is one dark cloud hanging over Alphabet, and it's the main reason its stock is so cheap compared to the rest of the Magnificent Seven. The U.S. Department of Justice (DOJ) won a major court case this year, finding that the company engages in monopolistic practices to protect its dominance in the internet search industry.

The judge won't hand down Alphabet's punishment until mid-2025, but the DOJ wants the company to sell its Chrome internet browser, and maybe even its Android operating system, to eliminate some of the distribution channels it uses to maintain Google Search's market share. Those measures would certainly harm Alphabet, but on the flip side, it's also possible the company is hit with a simple fine instead.

Many tech analysts predict this case will be tied up in the courts for years as Alphabet goes through the appeals process. As a result, it will be business as usual for now, so investors might be better off focusing on the company's efforts in the AI space.

Wall Street's consensus forecasts (provided by Yahoo) suggest Alphabet will generate record-high revenue and earnings in 2025. I'm not suggesting its stock will rise enough to trade in line with the average P/E ratio of the Magnificent Seven (which is 50.4). But even if it aligns with the 34.9 P/E ratio of the Nasdaq-100 technology index, that implies an upside of 38% from here, which would almost certainly be enough to beat the S&P 500 in 2025.

The case for Meta Platforms

Meta Platforms stock is up by almost 80% this year, yet it's still cheaper than most Magnificent Seven stocks. I think it will carry its momentum into 2025 for a few reasons, but they mostly relate to the company's efforts in the AI space.

The content feeds within Meta's Facebook and Instagram social networks are increasingly powered by AI. People will usually spend more time on those platforms if Meta can show them more of the posts they enjoy viewing, which means they see more ads and generate more revenue for the company. During the third quarter of 2024 (ended Sept. 30), CEO Mark Zuckerberg said AI-powered recommendations have driven an 8% increase in the amount of time users spend on Facebook this year and a 6% increase for Instagram.

Meta also launched an assistant called Meta AI last year, and it's now available in each of the company's apps. It can answer complex questions, generate images, offer ideas for fun activities with your friends, and even settle debates in your group chat. It already has more than 500 million monthly active users, and while it's free to use, there will be opportunities to monetize it in the future. For example, businesses might pay money to place a product link within Meta AI's response to a relevant question.

Meta AI is powered by Llama, a family of LLMs that Meta developed in-house. Llama is open source, so millions of developers regularly dig through the code, which allows Meta to rapidly identify bugs and ship improvements more quickly. So far, Llama has been downloaded more than 600 million times, making it the most popular family of open-source LLMs in the world.

Meta plans to launch Llama 4 next year, which Zuckerberg hopes will be the most powerful in the industry. The company is on track to spend up to $40 billion on AI data center infrastructure this year in order to build enough computing capacity to bring Llama 4 to life. Simply put, bigger LLMs lead to smarter AI software, so Meta hopes its investments will pay off over the long term by creating new opportunities to generate revenue through features like Meta AI.

Despite the strong gain in Meta stock this year, it would have to rise by another 19.5% in order for its current P/E ratio of 29.2 to match the 34.9 P/E ratio of the Nasdaq-100. Wall Street also thinks Meta will grow its earnings per share by 12% in 2025, which could pave the way for even more upside in its stock. With all of that in mind, I think it's a great candidate to beat the S&P 500 next year.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $342,278!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $47,543!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $496,731!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.