New

2 Technology Stocks That Could Help Make You A Fortune

Technology stocks have delivered healthy gains to investors in 2024 despite bouts of volatility, which is evident from the 14% gains clocked by the Nasdaq-100 Technology Sector index so far this year, though it is worth noting that the index has underperformed the S&P 500 index's 27% gains.

However, a look at the bigger picture will tell us that tech stocks have tended to outperform the S&P 500 index. For instance, the Nasdaq-100 Technology Sector has gained an impressive 364% over the past decade as compared to the 199% jump clocked by the S&P 500 over the same period. This outperformance can be attributed to tech companies' ability to capitalize on disruptive trends that can help them clock faster growth than non-technology companies.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

That's why buying and holding solid tech companies for the long run can help investors make a fortune. We will take a closer look at two such names in this article that could help substantially increase investors' wealth in the future.

1. Snowflake

Data cloud platform provider Snowflake (NYSE: SNOW) has witnessed a solid surge in its stock price lately thanks to the company's improving growth prospects that point toward better financial performance in the future. The company's data cloud offering allows customers to consolidate their data on a single platform, and they can then use that data for analytics, to build applications, or to gain insights.

The growing adoption of artificial intelligence (AI) has unlocked a new growth opportunity for the company. Customers are now purchasing AI-focused applications from Snowflake, using its offerings for purposes such as extracting data from text, summarizing text, creating chatbots, and searching data within text, among others.

Snowflake management points out that its AI-specific applications allow users to save 30% in cost as compared to other services while also helping them save 4,000 hours of manual tasks. The good part is that Snowflake is looking to push the envelope by offering more data cloud AI services. For instance, it has signed an agreement with Anthropic to give its customers access to new AI models on the Snowflake platform, which they can use to create chatbots, generate code, extract visual data, and automate processes, among other things.

More importantly, Snowflake's AI offerings are helping the company win a bigger share of its customers' wallets, apart from helping it attract new customers. For instance, Snowflake's total customer count jumped 20% year over year in the previous quarter to 10,618. However, the number of customers who have generated more than $1 million in product revenue for the company over the trailing 12 months increased at a stronger pace of 25% year over year.

Snowflake's net revenue retention rate of 127% is another proof of the increasing adoption of the company's offerings. A reading of more than 100% in this metric suggests that Snowflake's existing customers have increased the adoption of the company's solutions, as it compares the spending by its customers at the end of a period to the spending by those same customers in the year-ago period.

The combination of higher spending by Snowflake's existing customers, the addition of new customers, and the bigger deals that it is signing (as evident from the jump in the number of $1 million-plus customers) explain why its remaining performance obligations (RPO) shot up a remarkable 55% year over year last quarter to $5.7 billion. As this metric refers to the total value of a company's contracts that will be fulfilled in the future, its big jump indicates that Snowflake is set for faster growth in the future.

Not surprisingly, analysts have increased their earnings expectations from Snowflake and are expecting an acceleration in its bottom line going forward.

SNOW EPS Estimates for Current Fiscal Year data by YCharts

Moreover, Snowflake seems capable of sustaining its impressive momentum for a long time to come, as it expects its total addressable market (TAM) to double over the next five years, hitting $342 billion in 2028. All this makes Snowflake a top tech stock to buy for the long haul as the potential improvement in its growth could pave the way for solid upside in the long run.

2. Meta Platforms

Meta Platforms (NASDAQ: META) is known for operating famous social media apps such as Instagram, Facebook, Messenger, and WhatsApp, and this puts the company in a terrific position to capitalize on secular growth trends such as digital advertising and AI.

For instance, the size of the global digital ad market is expected to exceed $1.15 trillion by 2030, growing at an annual rate of 15% through the end of the decade. Meta Platforms is making the most of this fast-growing opportunity, clocking impressive growth this year. The company's revenue in the first nine months of 2024 increased by 22% from the same period last year to $116.1 billion. Its bottom line grew at a faster pace of 66% during the same period to $15.88 per share.

This suggests that Meta is growing at a faster pace than the digital ad market. That's not surprising considering the popular social media and messaging apps in the company's portfolio, which have allowed it to build a terrific user base. For instance, the number of daily active people using Meta's family of apps stood at 3.29 billion last quarter, up 5% from the year-ago period.

Throw in the fact that the integration of AI tools into Meta's advertising offerings is driving greater returns for advertisers, and it is easy to see why the company is witnessing an improvement in ad pricing and ad impressions. For example, advertisers using Meta's Andromeda machine learning (ML) tool have witnessed an 8% improvement in the quality of ads that advertisers have been able to deliver.

The company also points out that advertisers deploying its Advantage+ tool, which enables them to target audiences with the help of AI, has led to a 22% jump in returns on spending. As a result, there is a solid chance that Meta will be able to keep growing at a faster pace than the digital ad market for a long time to come.

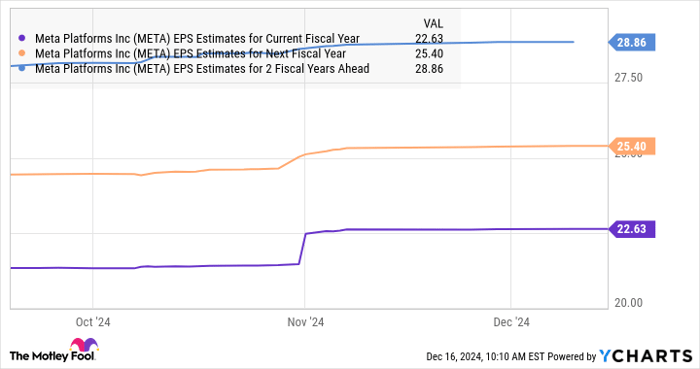

Not surprisingly, there has been a jump in analysts' growth expectations from Meta for the current and the next two years.

META EPS Estimates for Current Fiscal Year data by YCharts

However, it won't be surprising to see Meta clocking faster growth as tools such as AI could help it corner a bigger share of the digital ad market going forward. That's why investors can consider buying Meta Platforms while it is trading at an attractive 25 times forward earnings right now as compared to the tech-laden Nasdaq-100 index's forward earnings multiple of 28, especially considering that its massive addressable market could help it sustain its impressive growth for years to come and make investors richer in the process.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $790,028!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and Snowflake. The Motley Fool has a disclosure policy.