New

3 Dividend Stocks Up 8%, 16%, And 17% So Far In 2024 To Buy In December

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

2024 is almost over, but there's still time left in the year to identify quality companies that are worth buying now. Some folks may be looking for high-octane growth stocks with room to run, whereas others may be in search of companies that can pay them dividend income no matter what the stock market is doing.

Dividend stocks offer a way to participate in the market without all of the gains depending on the stock price going up. Investors can use dividend income to reinvest in the stock market, which can compound wealth over time.

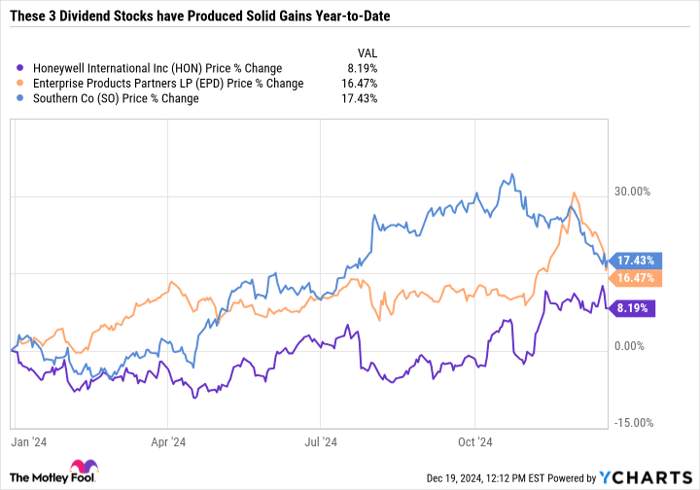

Honeywell International (NASDAQ: HON), Enterprise Product Partners L.P. (NYSE: EPD), and Southern Company (NYSE: SO) have rewarded investors with gains and dividend income, rising 8%, 16%, and 17% respectively so far this year. Here's why these three dividend stocks stand out as great buys in December.

Image source: Getty Images.

There's significant value to be released in a breakup of Honeywell

Lee Samaha (Honeywell): Industrial conglomerate Honeywell is about to join the industrial breakup party, which has been raging for the last half-decade. Peers like United Technologies (which spun off into Otis Worldwide, Carrier Global, and a merger with Raytheon Technologies to become RTX), General Electric (now GE Aerospace, GE HealthCare Technologies, and GE Vernova), and myriad other smaller conglomerates have all gone down that route. Honeywell's latest announcement strongly suggests it will take the same option.

The company announced its board of directors is continuing its portfolio evaluation "including the potential separation of its Aerospace business." The action is in line with calls for a breakup from an activist investor and makes sense given the elevated valuations in the aerospace sector -- Honeywell's largest business.

In addition, the company has already announced it will spin off its advanced materials business in 2025 or 2026 and has agreed to sell its personal protective equipment business for $1.325 billion in cash.

Moreover, other parts of Honeywell's portfolio of businesses, including industrial automation, building automation, and a 54% stake in the quantum computing business, Quantinuum, are positioned in highly attractive end markets.

For example, another industrial company, Emerson Electric, has restructured its portfolio to focus on automation, and Johnson Controls is also restructuring to focus on commercial building automation. The portfolio actions promise to release value for shareholders, and investors can earn a current dividend yield of 1.9% (a figure above the S&P 500 average of 1.3%) while they await updates.

Enterprise Products Partners is a cash-flow machine that's committed to rewarding investors

Scott Levine (Enterprise Products Partners): Shares of Enterprise Products Partners may have soared more than 16% since the start of the year, but don't let the pipeline stock's rise fool you, as it still seems reasonably priced.

Between the price tag and the 6.7% forward dividend yield, Enterprise Products Partners presents a great way for income investors to bolster their passive income streams.

Branding itself as a "fully integrated midstream energy company," Enterprise Products Partners operates more than 50,000 miles of pipelines as well as 20 deepwater docks and assets that provide liquids storage capacity over 300 million barrels. While some investors may balk at the stock's high dividend yield, a better understanding of the company's business should assuage the fears of those who are skeptical that the payout is sustainable. Because Enterprise Products Partners frequently signs long-term contracts with customers, management has excellent insight into future cash flows, helping it plan for capital expenditures. In addition, more than 90% of the company's long-term contracts have provisions to lessen the effects of inflation.

For 26 consecutive years, Enterprise Products Partners has hiked its payout, illustrating a steadfast commitment to returning capital to investors. And it's not as if management has imperiled the company's financial well-being to make investors happy. Over the past 15 years, for example, Enterprise Products Partners has averaged a distribution coverage ratio of about 1.5. Further evidence of the company's strong financial position comes from S&P Global Ratings, Fitch, and Moody's assignments of investment grade credit ratings. With shares trading at 10.8 times forward earnings, today seems like a great time to power your portfolio with Enterprise Products Partners stock.

The pullback in Southern Company is a buying opportunity

Daniel Foelber (Southern Company): Southern Company is still up big on the year but is down over 6% in the last month -- tumbling in lockstep with a broader sell-off in the utility sector. The sell-off has pushed Southern Company's dividend yield up to 3.5%, making it a compelling passive income opportunity for patient investors.

Southern Company has electric operating companies in the Southeastern U.S., natural gas distribution and utilities, and power generation facilities across the U.S. in wind, solar, and natural gas. Southern Company has invested heavily in nuclear energy, operating eight plants, including Vogtle Units 3 and 4, which are the first nuclear units to reach commercial operation in the U.S. in the last 30 years.

Southern Company's diversified portfolio of electric utility and power generation assets gives the company stable cash flows that can support dividend raises. Southern Company's dividend has roughly doubled over the last 20 years, which isn't too fast of a growth rate, but it has raised its dividend every year during that period.

Southern Company works with government agencies to set prices for customers, which limits profits but provides stability no matter what the economy is doing. In this vein, utility stocks like Southern Company can be good choices for risk-averse investors looking to generate passive income in retirement.

Southern Company's portfolio of fossil fuels, wind, and solar, and its experience with nuclear energy make it especially appealing for folks who believe in a balanced energy mix. With a 20.4 forward price-to-earnings ratio, Southern Company isn't a particularly expensive stock, making it a solid choice in December.

Should you invest $1,000 in Honeywell International right now?

Before you buy stock in Honeywell International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Honeywell International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $825,513!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Emerson Electric, GE HealthCare Technologies, Johnson Controls International, Moody's, and S&P Global. The Motley Fool recommends Enterprise Products Partners, GE Aerospace, and RTX. The Motley Fool has a disclosure policy.