New

Adobe Shares Sink Despite Record Revenue. Should Investors Buy The Stock On The Dip?

Despite posting record revenue to close out its fiscal year ended Nov. 29, shares of Adobe (NASDAQ: ADBE) were sinking as investors were disappointed with the company's guidance. Adobe has been at the forefront of generative artificial intelligence (AI) with both its Creative Cloud suite of products that includes Photoshop, and with its Document Cloud business featuring Acrobat. However, its monetization strategy related to AI has been a bit behind.

With its latest dip, the stock is now down about 18% year to date as of this writing. Let's take a close look at its results to see if this is a buying opportunity for investors going into 2025.

Record revenue, but disappointing guidance

Adobe closed out its fiscal year showing solid growth, with revenue increasing 11% to $5.61 billion. That was solidly ahead of its prior guidance calling for revenue of between $5.5 billion to $5.55 billion. Its adjusted earnings per share (EPS), meanwhile, jumped nearly 13% to $4.81, ahead of its $4.63 to $4.68 forecast.

Among its individual segments, Digital Media, which is home to both its Creative and Document Cloud businesses, saw revenue rise 12% to $4.15 billion. Within the segment, Document Cloud led the way with revenue jumping 17% to $843 million. Its larger Creative business saw revenue rise by 10% to $3.30 billion.

The company generated $578 million in new Digital Media annualized recurring revenue (ARR), ending the quarter with Digital Media ARR of $17.33 billion. That was just 2% growth from the $569 million in new Digital Media ARR it generated last year.

Adobe continued to hype its AI tools, saying AI image generations from its Firefly AI model continue to accelerate and have now crossed 16 billion cumulative generations. It recently launched its Firefly video model in beta, saying it saw massive interest in it, and it should be more broadly available in early 2025.

Image source: Getty Images.

Adobe's Digital Experience segment, which is involved in digital analytics and online marketing, saw its revenue increase by 10% to $1.4 billion, with digital experience subscription revenue jumping 13% to $1.27 billion. The company said it is seeing strong demand for its new Adobe GenStudio for Performance Marketing.

While the quarter itself was solid, what disappointed investors was Adobe's guidance. For the fiscal year 2025, the company projected revenue of between $23.30 billion to $23.55 billion, representing growth of between 8% to 9%. That was below the analyst consensus, as compiled by LSEG, looking for revenue of $23.78 billion. It guided for adjusted EPS of between $20.20 and $20.50.

For the fiscal first quarter, the company guided toward a revenue range of $5.63 billion to $5.68 billion, up from $5.18 billion a year ago and representing 9% to 10% growth. That was below the $5.73 billion analyst consensus. It's looking for adjusted EPS of between $4.95 to $5.

Below is a chart of the company's fiscal Q1 and full-year guidance.

| Metric | Fiscal Q1 Forecast | Fiscal Year 2025 Forecast |

|---|---|---|

| Revenue | $5.63 billion to $5.68 billion | $23.30 billion to $23.55 billion |

| Digital Media segment revenue | $4.17 billion to $4.20 billion |

$17.25 billion to $17.4 billion

|

| Digital Experience segment revenue | $1.38 billion to $1.40 billion |

$5.8 billion to $5.9 billion

|

| Adjusted earnings per share | $4.95 to $5.00 | $20.20 to $20.50 |

Data source: Adobe earnings releases.

Is the stock a rebound candidate?

Adobe's stock has underperformed this year, and despite all of Adobe's talk of AI innovation, that innovation has not translated into accelerating revenue growth. Creative Cloud, its largest business, saw new ARR increase just 2% in the quarter, while it forecast decelerating revenue growth for 2025.

The company is trying to balance drawing in new AI users versus its monetization of AI at the moment. That is currently leading to solid growth, but it hasn't lifted its revenue growth rate, which is what investors want to see. And while Adobe likely issued somewhat conservative guidance that it can beat, it gave no indication that its revenue growth could accelerate next year.

Adobe has been using a credit model for using generative AI, and its biggest AI opportunity may be moving away from this model. On the call, the company mentioned that it has the opportunity to create more tiers across its Creative products, and that will likely be the better way to monetize its AI efforts.

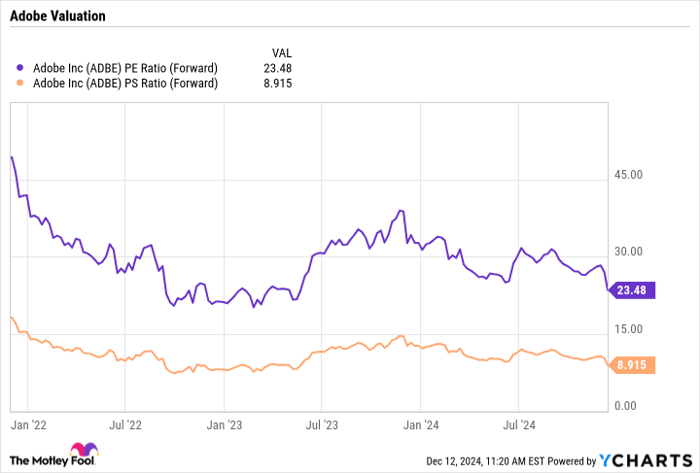

From a valuation standpoint, the stock currently trades at a forward price-to-earnings (P/E) ratio of 23.5 times fiscal year 2025 analyst estimates and a forward price-to-sales (P/S) multiple of under 9. That seems like a relatively attractive valuation.

ADBE PE Ratio (Forward) data by YCharts.

While I think Adobe still has a lot to prove, I like its product innovation roadmap, with things like Firefly video. More importantly, I think it can find a better monetization model through tiered plans. For this reason, I think investors can consider buying the dip in the stock.

Should you invest $1,000 in Adobe right now?

Before you buy stock in Adobe, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Adobe wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $822,755!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 9, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe. The Motley Fool has a disclosure policy.