New

Broadcom Joins The $1 Trillion Club: Is This Growth Stock A Buy Before The End Of The Year?

Nvidia (NASDAQ: NVDA) led the semiconductor industry and the tech sector to new heights in 2023 and 2024. The chipmaker embodied the breakneck pace of growth in the artificial intelligence (AI) sector, and has been trading the crown of most valuable company in the world with Apple and Microsoft. But it is far from the only chip stock that is putting up monster gains.

After reporting its fiscal 2024 fourth-quarter (ended Nov. 3) results on Dec. 12, Broadcom (NASDAQ: AVGO) surged by 24.4% on Dec. 13 to a new all-time high and a market cap of $1.05 trillion. The stock has more than doubled year-to-date and is now up by more than 600% during the past five years. In fact, Nvidia is up just 1% during the past six months, while Broadcom has surged by about 44% (as of Dec. 16).

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Here's what you need to know about the tech giant's results, where it could be headed, and if this growth stock is worth buying before 2025.

Image source: Getty Images.

A primer on Broadcom

Broadcom is in the business of global connectivity. It provides hardware and software solutions for cloud infrastructure, data centers, networking, broadband, wireless, storage, industrial applications, enterprise software, and more.

The company makes equipment for advanced ethernet switching, which it believes will be in higher demand from hyperscalers like Amazon Web Services. Another big opportunity for Broadcom is application-specific integrated circuits (ASICs) for data centers. It has a majority share of the ASIC market, which could see surging demand as businesses look for lower-cost alternatives to Nvidia's GPUs.

Broadcom is unique because it has an integrated portfolio of products across the data center value chain, including network, server, and storage connectivity. It's thus a catch-all way to play the need for increased connectivity and AI.

Blowout results

The rises of cloud computing, infrastructure, and AI have transformed Broadcom from a value-focused company to a high-octane growth stock. Its market cap surged due to increased demand from these industries.

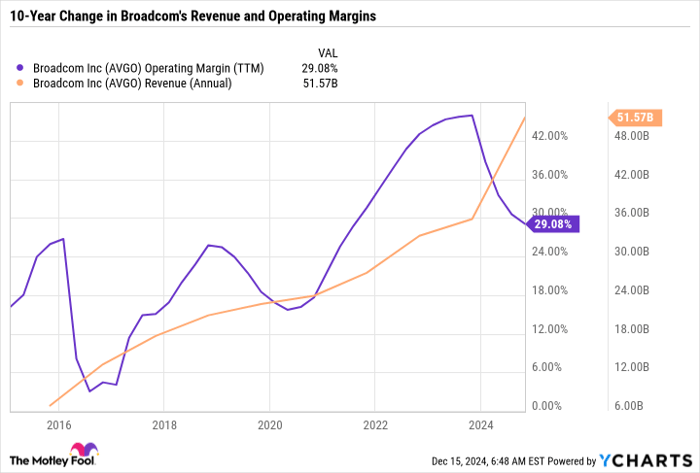

The following chart shows the company's margin expansion and its revenue growth, which is up nearly eightfold during the past decade and a whopping 44% in fiscal 2024 compared to fiscal 2023. The recent narrowing in margins is largely due to the adjustments related to Broadcom's purchase of VMware and because it is investing heavily in innovation, not due to price sensitivity.

AVGO Operating Margin (TTM) data by YCharts.

Management sees the momentum carrying forward into fiscal 2025, forecasting first-quarter revenue of $14.6 billion and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of $9.64 billion. If it hits those targets, its revenue would increase by 22% year over year and adjusted EBITDA by 35%. Since the acquisition of VMWare somewhat inflated Broadcom's fiscal 2024 results, its fiscal 2025 growth will provide a more accurate reading of the company's post-acquisition growth rate.

Broadcom's transformation

Broadcom closed on its blockbuster purchase of VMware in early fiscal 2024. The deal boosted its position in software, cloud, and data centers, but there were questions about how fast it could integrate the organization. On the recent earnings call, management said that the integration of VMware was largely complete, and it is ahead of schedule on its sales and earnings growth. Chief Executive Officer Hock Tan attributed the integration of VMware and AI growth as the two significant drivers of Broadcom's transformations in fiscal 2024:

Our AI revenue, which came from strength in custom AI accelerators or XPUs and networking, grew 220% from $3.8 billion in fiscal 2023 to $12.2 billion in fiscal 2024, and represented 41% of our semiconductor revenue. This drove semiconductor revenue up to a record $30.1 billion during the year.

AI has emerged as a key driver of semiconductor revenue, now Broadcom's largest segment by revenue, with momentum continuing in the near term. But that news alone likely wouldn't have resulted in the more than $200 billion pop in Broadcom's market cap in a single session. That pop more likely came because of management's three-year forecast.

Broadcom sees its three big hyperscale customers developing their own customer AI accelerators or XPUs over a multiyear period to represent a serviceable addressable market of $60 billion to $90 billion by fiscal 2027. Broadcom expects to dominate that market, and anticipates that its AI-driven semiconductor business will eclipse its non-AI semiconductor business in the near future. If it meets its targets, it would be the equivalent of Apple releasing a new product that became bigger than the iPhone in just five years.

Expectations are high

Not long ago, it was easier to value Broadcom based on its trailing earnings and its growing dividend (which it just raised by 11%). But given how much the business has changed in a short amount of time, it is entering a new territory -- valuation expansion.

Valuation expansion occurs when investors are optimistic about a company's growth and are willing to value it based more upon its expected future earnings than on those of its recent past. Analysts' average expectations are for Broadcom's earnings to soar in the coming year, so the stock only sports a forward price-to-earnings ratio of 36. That's surprisingly cheap for a stock that doubled during the past year and is up more than sevenfold in the past five years. But projections can differ from results, especially in the highly cyclical semiconductor industry.

Broadcom's valuation is being put to the test

The investment thesis for Broadcom used to be that it was an established network connectivity business that was well-positioned to monetize AI. But in just one year, the company caught Wall Street off-guard by essentially stating that the AI-related semiconductor segment will become its largest. This fundamental change is reminiscent of the evolution of Nvidia -- its graphics segment used to be bigger than its data center business, but now, the data center business accounts for 85% of revenue.

Broadcom remains an excellent buy if you believe in management's vision for capturing hyperscaler spending on AI. If it comes even close to its medium-term targets, future investors will likely be looking back on the current share price as a good value.

However, the stock could also sell off big time if an industrywide downturn occurs or if its forecasts are too optimistic. After all, management warned that the ramp-up in hyperscaler investment will not be linear, with outlays potentially varying widely from quarter to quarter.

Therefore, investors should take care to weigh the risks and potential rewards before jumping into Broadcom after its recent run-up. Some may want to wait and see how the hyperscalers' infrastructure ramp-up plays out. Today, the stock is priced for results that are close to perfection, but if there are hiccups along the way, it could come down to a more attractive valuation.

Should you invest $1,000 in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $808,966!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.