New

Can C3.ai Become The Next Palantir Technologies?

Palantir Technologies (NASDAQ: PLTR) stock was in red-hot form in 2024 as investors showed increasing interest in this software platforms specialist thanks to strong demand for the company's artificial intelligence (AI)-focused offerings, which led to nice accelerations in its top- and bottom-line growth.

As of this writing, the stock is up an eye-popping 380% this year, and now trades at an extremely rich valuation. With a price-to-sales ratio of 75 and a trailing earnings multiple of 412, Palantir is not an ideal candidate for investors looking to buy an artificial intelligence (AI) stock at a reasonable valuation.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

Of course, the forward earnings multiple of 217 indicates that the company's bottom line is expected to improve remarkably in the coming year, but that rich valuation also means that any signs of weakness in Palantir's growth story could send the stock spiraling downward. There is a good chance that Palantir can sustain its impressive growth in the long run considering the lucrative AI software platforms market that it is serving, but it's still a risky investment.

Those looking for a more reasonably priced company that's trying to capitalize on this opportunity might want to consider C3.ai (NYSE: AI). Its stock notched more modest gains of 23% in 2024 and has been in the news for the wrong reasons of late. But it's also trading at significantly cheaper valuations than Palantir and is tapping a similar addressable market. As such, now would be a good time to ask if C3.ai can follow in its bigger peer's footsteps and deliver eye-popping gains to investors.

Plenty of room for growth in AI software

According to market research firm IDC, the AI software platforms market generated $28 billion in revenue in 2023. The firm forecasts that this market could be worth a whopping $153 billion by 2028, which means that there is room for more than one company to thrive in this space. Both Palantir and C3.ai are thus far just scratching the surface of a massive opportunity.

Palantir's revenue over its past four reported quarters was $2.65 billion. C3.ai, on the other hand, generated $325 million. More importantly, both companies saw upticks in their growth rates since the beginning of 2023.

PLTR Revenue (TTM) data by YCharts.

What's more, both companies reported almost identical growth rates in their latest quarters. While Palantir's revenue increased 30% year over year to $726 million in the third quarter of 2024 to $726 million, C3.ai's top line jumped 29% year over year to $94 million in its fiscal 2025 second quarter, which ended on Oct. 31.

Both also increased their full-year revenue guidance as the demand for their generative AI software solutions increased among both commercial and government customers. It is worth noting that Palantir initially made its name by supplying software platforms and analytics solutions to U.S. government agencies, but it has lately been focusing on winning more commercial customers in the enterprise AI software space.

A similar story is unfolding at C3.ai. The company has "entered into new and expanded agreements with the U.S. Department of Defense, the U.S. Air Force, the U.S. Navy, the U.S. Army, the U.S. Marine Corps, the Defense Logistics Agency, and the Chief Digital Artificial Intelligence Office, among others," CEO Tom Siebel said the latest earnings conference call.

Meanwhile, C3.ai has partnered with major cloud service providers such as Microsoft, Amazon, and Google to ensure a broader reach for the 100-plus enterprise AI applications that it offers. The company also offers an enterprise AI application development platform that allows customers to build their own solutions, apart from industry-specific solutions that help customers integrate generative AI into their operations.

The company, in short, seems to be positioning itself to make the most of the huge addressable opportunity in the AI software market. But will that be enough for it to succeed to the degree that Palantir has?

Strong growth is in the cards for both companies

C3.ai is currently a much smaller company than Palantir. However, its top-line growth was almost the same as Palantir's last quarter, and both companies have enjoyed an uptick in their growth in the past couple of years.

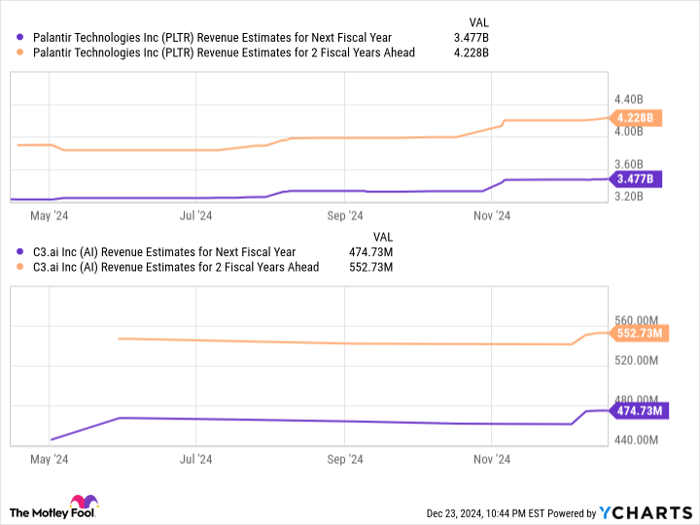

In addition, both companies expect to report a 25% increase in their top lines in the current fiscal year. Palantir's revenue is expected to land at $2.79 billion in 2024, while Palantir is expected to clock $388 million in revenue in the current fiscal year. Analysts anticipate robust double-digit percentage growth over the next couple of years as well.

PLTR Revenue Estimates for Next Fiscal Year data by YCharts.

Even better, analysts have increased their growth expectations from both companies. That's not surprising considering the size of the markets they serve, and there is a good chance that their growth prospects could continue improving as the adoption of generative AI software increases.

So, even though C3.ai is expected to remain a smaller company than Palantir over the next couple of years, its solid growth and end-market opportunities make it an ideal alternative for anyone looking to benefit from the growth of the AI software market at a reasonable valuation.

After all, C3.ai's sales multiple of 13 is less than a fifth of its bigger counterpart, even as their growth rates are almost equal. That's why investors looking for the next Palantir would do well to keep C3.ai on their watch lists or buy it now, as its improving growth profile could lead to healthy share price gains.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $363,593!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $48,899!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $502,684!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 23, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Microsoft, and Palantir Technologies. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.