New

Do Older Adults Understand Healthcare Risks?

Misperceptions of long-term care needs and costs are cause for concern.

Households approaching retirement face a wide variety of risks to their financial security. They may live longer than planned and deplete their resources; they may experience unexpectedly high inflation; or they may receive unusually poor returns on their investments. Equally consequential is the risk that households will face major expenses to cover medical and long-term care costs. My colleagues and I just completed a study based on a new survey to determine the extent to which older adults understand the risks they face.

The focus of our concern was primarily the costs associated with long-term care. Of course, medical risks are highly uncertain and potentially expensive, but much of this risk is insured by Medicare (and Medicaid for those eligible for both programs).

Long-term care risks, in contrast, are not well insured. Only 3 percent of all U.S. adults or 15 percent of those ages 65+ have long-term care insurance, and Medicaid, the public insurance program targeted at low-income individuals, is not a realistic option for most middle-income families.

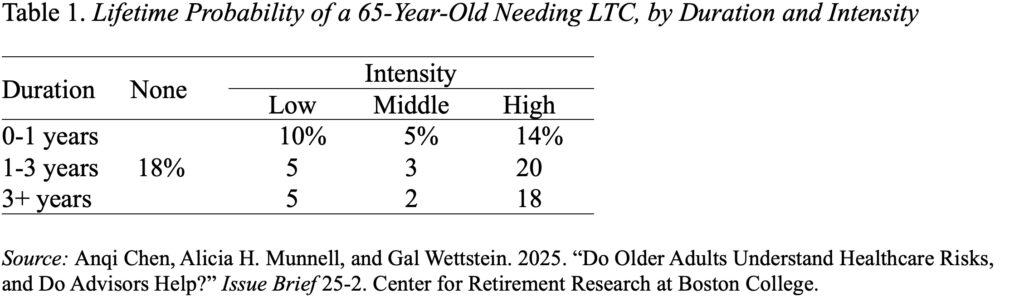

Yet, 80 percent of 65-year-olds will need long-term care at some point over their remaining life (see Table 1). And while the intensity and duration of these long-term care needs vary substantially, about 40 percent will require high-intensity care for more than a year.

Given the extensive needs and lack of insurance, family members often cover the majority of care hours for people with low and moderate needs and supplement the efforts with paid caregivers as needs increase. Paid LTC, however, is very costly – in 2023, the median annual costs were $116,800 for a private room in a nursing home, $75,500 for home health aides, and $64,200 for an assisted living facility.

To look at households’ perceptions regarding healthcare risks, Greenwald Research interviewed online 508 individuals ages 48-78 with at least $100,000 in investable assets in July 2024. The results showed that medical and long-term care needs were low on most respondents’ list of concerns (see Figure 1) – a finding consistent with other studies.

Moreover, only 39 percent of older households could correctly estimate the cost of a nursing home, 34 percent for home care services, and only 15 percent for assisted living facilities (see Figure 2).

One reason that households have such big misperceptions about both the risks and the costs of long-term care is that survey after survey has found that many mistakenly believe that Medicare covers LTC. The most recent example from KKF shows that 45 percent of respondents ages 65+ think that Medicare will pay for their LTC and another 9 percent think that their costs will be covered by private health insurance (see Table 2).

Underestimating healthcare risks – particularly the risks of long-term care needs – has real costs. Households do not purchase long-term care insurance nor save in advance for such an event. Instead, they are left on their own with inadequate resources to navigate a very demanding, complicated, and costly challenge.