New

Down 22%, Here's How Adobe Could Follow In Salesforce's Footsteps To Become A Strong Buy In 2025

With just a few weeks left in the year, the tech sector is shaping up to, once again, beat the S&P 500 (SNPINDEX: ^GSPC) largely thanks to gains from Nvidia and Broadcom in the semiconductor industry. The software industry also makes up a large share of the tech sector but has enjoyed mixed results on the year. For example, Salesforce (NYSE: CRM) is beating the S&P 500's year-to-date gain, but Microsoft and Adobe (NASDAQ: ADBE) are lagging behind. Adobe, in particular, is down over 22% year to date at the time of this writing -- heavily underperforming the sector.

Here's what Salesforce is doing right, why Adobe is out of favor, and whether either growth stock is worth buying now.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Image source: Getty Images.

Paths diverge

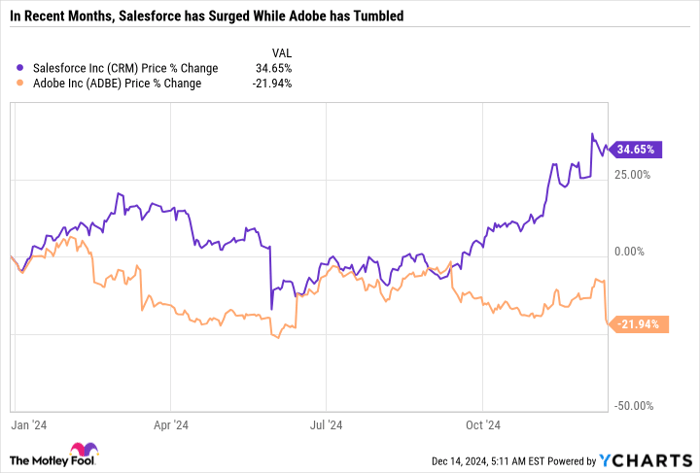

Not long ago, Salesforce was in the same boat as Adobe. Both companies were missing out on the broader tech sector rally as investors questioned if spending big bucks on artificial intelligence (AI) would pay off. However, as you can see in the chart, Salesforce has exploded higher in recent months, while Adobe is getting dangerously close to its 52-week low.

Salesforce has become a standout in the enterprise software space because it has a compelling AI opportunity that will immediately contribute to top- and bottom-line growth. The opportunity is what Salesforce calls AI agents, which rely on machine learning and natural language processing to answer questions, solve problems, and make decisions. Agentforce is the platform where organizations can customize and build multiple AI agents.

On Salesforce's third-quarter fiscal 2025 earnings call, the company mentioned the word "agent" a whopping 136 times. Typically, when a company over-emphasizes a new product or service, it can be a bit of a red flag that management is overpromising. However, given the rally in the stock price, investors seem to think Agentforce could be the real deal.

Agentforce is arguably Salesforce's most significant innovation in years and offers a clear path to contributing high-margin revenue to Salesforce right away. Launched in October, the service is usage-based and costs $2 per conversation. As my colleague Geoffrey Seiler points out, that's a $2 billion opportunity based on Salesforce CEO Marc Benioff's goal of having 1 billion AI agents by the end of fiscal 2026 (which would correspond to early calendar year 2026). For context, Salesforce is guiding for around $38 billion in revenue in fiscal 2025.

If Agentforce is successful, it could accelerate growth and differentiate the company's enterprise software suite, which includes Salesforce, Slack, Tableau, and more. However, for now, Salesforce is only guiding for 8% to 9% revenue growth in fiscal 2025 compared to fiscal 2024.

In sum, Salesforce may not be growing rapidly, but it has the AI-driven growth narrative in spades, which makes the stock intriguing for long-term investors.

Adobe investors remain skeptical of its future in AI

Adobe just reported fiscal fourth-quarter and full-year fiscal 2024 results, growing revenue by 10.8% year over year in the period ended Nov. 29. The company is guiding for accelerated revenue growth of 14.2% in fiscal 2025 and non-GAAP (adjusted) earnings-per-share growth of 10.5%. And yet, Adobe sold off by over 13% the session after reporting earnings.

Despite their similar near-term growth rates, investors are cheering Salesforce and have turned negative on Adobe. There is now widespread conviction that Salesforce's AI-fueled growth is the real deal, whereas there are doubts that Adobe can effectively monetize AI.

Adobe has developed many AI-fueled product upgrades and just notched another record year of high-margin growth. However, it has yet to deliver the show-stopping announcement that Salesforce gave with Agentforce.

Salesforce and Adobe: 2 growth stocks worth a closer look

The recent surge in Salesforce stock showcases investor excitement for AI-driven enterprise software solutions, while the disappointment in Adobe indicates a lack of patience for companies that don't have a clear roadmap for monetizing AI. As an individual investor, you don't have to get overly caught up in the short-term price action. Instead, it is better to filter out the noise and determine if a company has a runway for future growth and if the valuation makes sense.

Salesforce has had a big run-up, but there's undeniable potential with Agentforce that could still make the stock a good buy now. However, some investors may prefer to wait and see if Salesforce can deliver on its lofty targets before jumping in now.

Meanwhile, the sell-off in Adobe seems a little overblown. The midpoint of Adobe's non-GAAP fiscal 2025 earnings guidance is $20.35 per share, giving the company a forward price-to-earnings ratio of just 22.5. That's dirt cheap for a high-margin industry-leading cash cow that is poised for solid growth in the year to come.

Should you invest $1,000 in Salesforce right now?

Before you buy stock in Salesforce, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Salesforce wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $808,966!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Microsoft, Nvidia, and Salesforce. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.