New

Meet Wall Street's Newest $1 Trillion Artificial Intelligence (ai) Stock -- But Don't Rush To Buy It Just Yet

Up until the market opened on Friday, Dec. 13, America was home to seven technology companies worth $1 trillion or more:

- Apple: $3.7 trillion.

- Nvidia: $3.3 trillion.

- Microsoft: $3.3 trillion.

- Amazon: $2.4 trillion.

- Alphabet: $2.3 trillion.

- Meta Platforms: $$1.5 trillion.

- Tesla: $1.4 trillion.

However, an eighth company just joined the ranks. Broadcom (NASDAQ: AVGO) stock surged 24% last Friday following the release of its financial results for fiscal 2024 (ended Nov. 3), catapulting the company into the exclusive $1 trillion club.

Investors were impressed with Broadcom's soaring artificial intelligence (AI) revenue, which comes from selling custom chips and networking equipment for data centers. Plus, the company issued a very bullish forecast for its future AI revenue, which points to substantial potential growth ahead.

However, before you rush to buy Broadcom stock, you'll have to get comfortable with its lofty valuation. Here's what you need to know.

Broadcom is becoming a serious player in AI hardware

Broadcom was solely a supplier of semiconductors and electronics components for a variety of computing applications up until 2016, when it merged with fellow chip giant Avago Technologies. From there, the new-look Broadcom went on to spend around $100 billion acquiring other companies like semiconductor equipment supplier CA Technologies, cybersecurity vendor Symantec, and cloud software titan VMware.

Those companies helped Broadcom diversify its business, and they are now important contributors to the company's overall revenue. In other words, they paved the way for it to become the $1 trillion giant it is today. But thanks to the spending boom on AI infrastructure from some of the world's leading tech giants, investors are currently laser-focused on Broadcom's semiconductor and networking businesses.

The company makes custom AI accelerators (a type of data center chip) for three hyperscale customers, and while their identities are not disclosed, hyperscalers typically include Microsoft, Amazon, Alphabet, and Oracle. During Broadcom's fiscal 2024 fourth quarter, it said shipments of AI accelerators doubled compared to the year-ago period.

Here's why that's important. Nvidia's graphics processing units (GPUs) for the data center are currently the most sought after chips in the AI industry. While each of the above hyperscalers are Nvidia customers, Broadcom gives them the ability to design their own chips, which means they can tailor their infrastructure to their own specific needs -- not to mention significantly reduce costs (Nvidia's hardware is very expensive).

Additionally, the company said its AI connectivity revenue soared fourfold thanks to sales of its Tomahawk and Jericho data center switches. Those devices regulate how quickly data travels between chips and devices, and since AI developers often use tens of thousands of chips to train their models, faster processing can lead to substantial cost savings.

Image source: Getty Images.

AI revenue surged during fiscal 2024

Broadcom generated a record $51.5 billion in total revenue during the whole of fiscal 2024, which was a 44% increase from fiscal 2023. However, the majority of that growth was attributable to the inclusion of VMware's revenue for the first time, rather than organic growth (Broadcom acquired the company in 2023).

Nevertheless, Broadcom managed to impress investors with its AI revenue, which surged by a whopping 220% to $12.2 billion in fiscal 2024. Most of that came from sales of the AI accelerators and networking equipment discussed earlier, and the company expects to carry its strong momentum into fiscal 2025.

Broadcom's overall revenue growth came with a substantial increase in costs, which were partly attributable to the company's acquisitions (namely of VMware). Research and development spending, for example, increased by 78% year over year to $9.3 billion, which was the largest of the company's $19 billion in total operating expenses in fiscal 2024.

As a result, Broadcom's fiscal 2024 net income (profit) of $5.9 billion actually represented a decrease of 58% from fiscal 2023. That significantly impacts the valuation of Broadcom stock for any investor valuing it based on its GAAP earnings, which I'll discuss further in a moment.

On a non-GAAP basis, which excludes one-off expenses from acquisitions and non-cash costs like stock-based compensation, Broadcom's net income came in at $23.7 billion, which was actually a 28% increase from fiscal 2023. That gives investors a clearer idea of the trajectory of Broadcom's business.

Broadcom stock looks expensive right now

Broadcom generated GAAP earnings per share (EPS) of $1.23 during fiscal 2024, so its stock trades at a price-to-earnings (P/E) ratio of 183. That's an eye-popping number considering the Nasdaq-100 technology index trades at a P/E ratio of just 35.

Based on its non-GAAP EPS of $4.96, its P/E ratio is 45. While significantly better, it's still a big number relative to the broader tech sector. Plus, many investors don't consider non-GAAP EPS to be "true" profitability, so it isn't a good idea to hang your hat on that number to make the argument that Broadcom stock looks attractive.

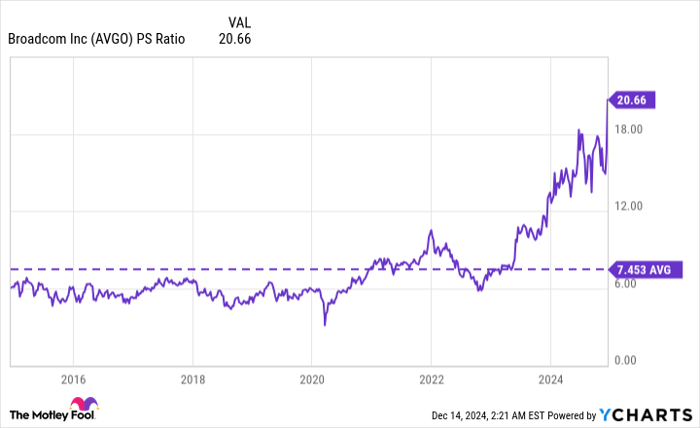

Rather than using the traditional P/E ratio, we could value Broadcom using the price-to-sales (P/S) ratio instead, which divides a company's market capitalization by its annual revenue. Broadcom's P/S ratio is currently 20.7, which is almost triple its 10-year average of 7.4:

AVGO PS Ratio data by YCharts

In other words, Broadcom stock looks very expensive based on two measures of its P/E ratio, and also its P/S ratio. Therefore, buying the stock right now probably isn't a great idea for short-term investors with a time horizon of 12 months.

However, there might be a compelling case to buy it for long-term investors who are willing to hold the stock for the next three years or more. That's because Broadcom thinks it can grow its AI revenue to between $60 billion and $90 billion annually by fiscal 2027, thanks to soaring demand for accelerators and networking equipment.

Remember, its AI revenue came in at just $12.2 billion in fiscal 2024, so we're talking about a whopping 514% increase over the next three years (at the midpoint of the range).

I still think investors should wait for a pullback before buying Broadcom stock given its current valuation, but it's certainly a very high-quality way to play the AI boom.

Should you invest $1,000 in Broadcom right now?

Before you buy stock in Broadcom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Broadcom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $822,755!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Oracle, and Tesla. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.