New

The Bull Market Continues: 1 Stock-split Stock To Buy As Part Of Your 2025 New Year's Resolution

High-quality companies tend to create lots of value for their shareholders over the long term. Sometimes, that means their stock price soars into the hundreds or even thousands of dollars, which can make it difficult for retail investors to buy in.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

Companies can remedy that with a stock split, multiplying the number of shares they have in circulation while simultaneously reducing the stock price proportionately. For example, a 10-for-1 stock split would increase a company's share count tenfold, and reduce its price-per-share to one-tenth of what it was previously.

These maneuvers don't change the value of the underlying company one bit -- the reduced share price is entirely cosmetic. A split just makes it easier for small investors to buy into a business.

Image source: Getty Images.

2024 was a big year for stock splits

The S&P 500 (SNPINDEX: ^GSPC) is in a raging bull market right now, and it's showing no signs of slowing. Several high-profile companies saw significant increases in their stock prices throughout 2024, and completed stock splits to shrink them to more affordable levels:

- Nvidia completed a 10-for-1 split on June 10 that reduced its stock price from $1,200 to around $120.

- Chipotle completed a 50-for-1 split on June 26 that reduced its price-per-share from $3,283 to just $66.

- Broadcom completed a 10-for-1 split on July 12 that reduced its stock price from $1,700 to $170.

- Palo Alto Networks (NASDAQ: PANW) completed a 2-for-1 split on Dec. 13 that reduced its stock price from $400 to $200.

With 2025 right around the corner, now might be a great time for investors to explore new opportunities. The above stocks were some of the biggest value creators in 2024, and each of them is carrying solid momentum into the new year.

But Palo Alto presents a particularly interesting opportunity. It's a leader in the cybersecurity industry, and with cyber threats constantly on the rise, demand for its software is likely to continue climbing in 2025. Plus, the company is embedding artificial intelligence (AI) across its product portfolio, which is creating substantial amounts of value for both customers and shareholders.

So, here's why buying Palo Alto stock might be a great addition to your list of New Year's resolutions.

A leader in AI-powered cybersecurity

Palo Alto operates three cybersecurity platforms covering cloud security, network security, and security operations, each of which contains dozens of individual products. The company is embedding AI into as many of those products as possible in its efforts to help its clients eliminate threats faster and more accurately.

Large organizations typically have security operations centers that are staffed with analysts and experts who remediate cyber incidents. Palo Alto believes too many of those centers rely on human-led processes that are being overwhelmed by the frequency of modern attacks. That's why it launched Cortex XSIAM -- a security operations center platform powered entirely by AI that features more than 400 algorithms to prioritize automation.

XSIAM customers are having a lot of success. One oil and natural gas company reduced the number of cybersecurity incidents requiring human investigation by 75%, and a healthcare provider using it now resolves 90% of incidents with automation (up from 10% previously).

Organizations also face fresh risks when deploying AI into their operations. Many of them are plugging their sensitive data into third-party AI models (like those from OpenAI and Anthropic) to build software, which creates a new point of vulnerability. Palo Alto is working on a product portfolio called Secure AI by Design that it hopes will address some of those challenges. It could be a big growth driver as AI adoption expands.

Palo Alto's revenue growth is accelerating

The cybersecurity industry used to be extremely fragmented. Providers specialized in specific products, so businesses pieced their security stacks together from multiple vendors. Palo Alto changed that by becoming a true one-stop shop via its three platforms.

Palo Alto says the lifetime value of a customer that uses all three of its platforms is 40 times higher than the value of a customer using just one, so this strategy makes a lot of sense. The company started focusing on "platformization" around a year ago by offering customers fee-free periods to entice them to move away from other cybersecurity providers. That led to a temporary slowdown in its revenue growth, but the strategy is starting to pay off.

During its fiscal 2025 first quarter, which ended Oct. 31, Palo Alto generated $2.1 billion in total revenue. That was a 14% increase from the prior-year period, marking an acceleration from the 12% growth it delivered in its fiscal 2024 Q4.

Palo Alto also reported $4.5 billion in annual recurring revenue (ARR) from next-generation security (NGS) products at the end of Q1, which was a 40% increase from the year-ago period. Palo Alto describes NGS products as those that result from its substantial investments in innovation, so the AI products within the Cortex platform (like XSIAM, for example) fit into that bucket.

Moreover, the company says more than half of the customers contributing NGS revenue are "platformed," so the fact that this segment delivered 40% ARR growth really highlights the potential of platformization.

Why Palo Alto stock is a buy for 2025

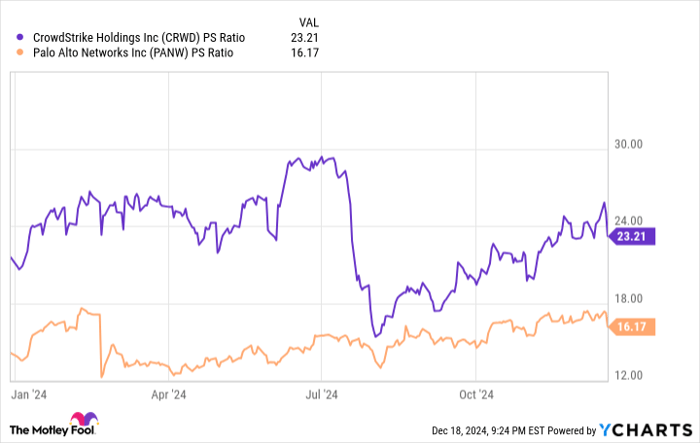

Palo Alto stock is up by 30% in 2024 and it's near a record high. However, it trades at a price-to-sales (P/S) ratio of 16.1, which is a cheaper valuation than its main competitor, CrowdStrike (NASDAQ: CRWD).

CRWD PS Ratio data by YCharts

CrowdStrike might deserve a bigger premium because it grew its total revenue by 29% in its latest reported quarter compared to Palo Alto's 14%. However, Palo Alto is a much larger provider. Its NGS ARR of $4.5 billion alone is more than CrowdStrike's total ARR of $4 billion. Plus, remember, its NGS revenue grew by 40% -- so maybe Palo Alto's P/S ratio deserves to be a little higher after all.

Palo Alto has 1,100 platformization customers right now, but it intends to grow that number to 3,500 by fiscal 2030, which could translate into NGS ARR of $15 billion. That would give Palo Alto stock a forward P/S ratio of 8.2, so its share price would have to nearly double over the next five years just for it to maintain its current P/S ratio of 16.1.

But demand for products like Secure AI by Design could be higher than management expects. A recent study by McKinsey and Company indicates that 72% of organizations have adopted AI in at least one business function, but only 8% are using it in five functions or more. In other words, adoption of this technology is still in an early stage, and businesses are going to need more cybersecurity tools to protect their sensitive data as they deploy AI more broadly.

Palo Alto will continue to roll out new products for the AI era during 2025, so given the company's current valuation relative to its chief competitor, it could be a great stock to own in the new year. And it's now more accessible for smaller investors thanks to its recent stock split.

Should you invest $1,000 in Palo Alto Networks right now?

Before you buy stock in Palo Alto Networks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palo Alto Networks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $790,028!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill, CrowdStrike, and Nvidia. The Motley Fool recommends Broadcom and Palo Alto Networks and recommends the following options: short December 2024 $54 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.