New

Up 4%, 10%, And 25% In 3 Months, These 3 Dow Jones Dividend Growth Stocks Are Buys In December

In contrast to the S&P 500 or the growth-fueled Nasdaq Composite, the Dow Jones Industrial Average is more value-focused. However, the Dow has become more growth-focused in recent years with the additions of Salesforce, Amazon, and Nvidia.

Still, the Dow is chock-full of industry-leading blue chip companies that pay dividends. At the time of this writing, Microsoft (NASDAQ: MSFT), Visa (NYSE: V), and Walt Disney (NYSE: DIS) are up 4%, 10%, and 25%, respectively, in the last three months. Here's why these companies have what it takes to grow their earnings and payouts for years to come.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

Image source: Getty Images.

Microsoft offers growth and passive income at a good value

The year 2023 was big for Microsoft. The stock surged 56.8% in response to several artificial intelligence (AI) developments, including Microsoft's role in OpenAI; the expansion of Microsoft Copilot, which became generally available to Microsoft 365 enterprise customers on Nov. 1, 2023, and advancements in AI for Microsoft Cloud and GitHub.

The stock has surged another 18.9% in 2024 but is lagging the S&P 500's year-to-date gain. In November, it had its worst day in two years in response to quarterly results that included increased spending on AI and lower near-term profit margins. The underperformance could present a buying opportunity for investors confident that Microsoft can continue monetizing AI and accelerating its growth.

Recently proposed changes to the contract structure between the company and OpenAI could remove some limitations, give Microsoft access to advanced technologies, and eliminate investor profit caps.

Microsoft is playing the long game with its AI investments, so investors should expect volatility depending on how Wall Street digests its quarterly performance. However, the company remains a balanced buy due to its exposure to several end markets and an impeccable balance sheet with more cash, cash equivalents, and marketable securities than debt.

It is an underrated dividend stock, having increased its payout for 15 consecutive years at a 13.2% compound annual growth rate. Its yield is low due to its outperforming stock price over that period, not a lack of commitment to the dividend.

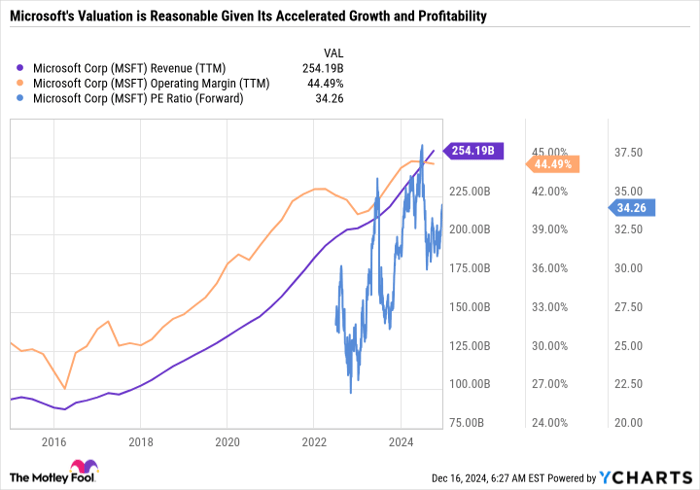

Microsoft has a forward price-to-earnings ratio (P/E) of 34.4, which is reasonable given that it is generating record-high sales and its highest operating margin in over a decade. The company's growth could accelerate further if it makes another breakthrough in AI.

MSFT revenue (TTM), data by YCharts; TTM = trailing 12 months.

Add it all up, and Microsoft stands out as arguably the most balanced mega-cap tech stock to buy in December.

Visa can stay a good value thanks to consistent stock repurchases

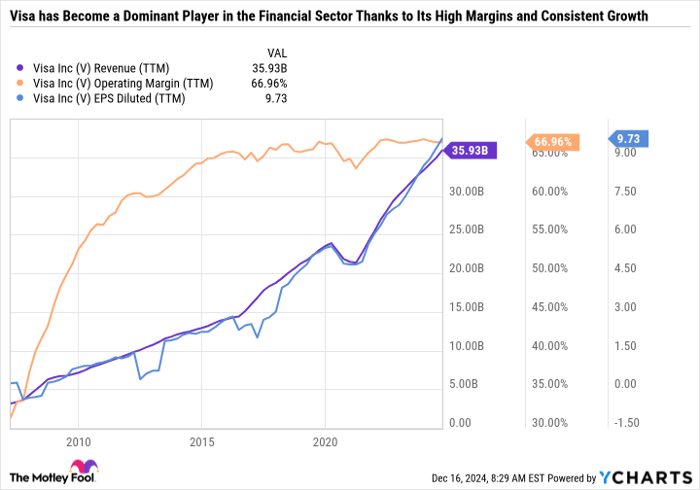

In the last five years, Visa's diluted earnings per share (EPS) are up 99%, sales are up 64.5%, and the company has maintained its ultra-high operating margins. The 20-year chart of key metrics highlights its unbelievable growth and consistency.

V revenue (TTM), data by YCharts.

Visa has been at the forefront of the transition from cash to digital payment processing, which forms the backbone of e-commerce and in-person point-of-sale. It has transformed into a global business, handling currency conversion and transactions for customers when they travel internationally.

Network effects are the key ingredient to the unstoppable business model. The network depends on customers using Visa debit and credit cards, and merchants accept those forms of payment. The larger the network grows, the more it is recognized and trusted -- giving customers greater incentive to use the cards as their primary form of payment and merchants to accept the transaction fees to grow their sales. Ideally, it's a win for all involved because of the network's reliability and security.

Like Microsoft, Visa's stock is hovering around an all-time high, but the stock is still a reasonable valuation -- with a forward P/E of 28.1. The company has raised its dividend payout every year since 2009, but it primarily returns capital to shareholders through buybacks. Stock repurchases have been instrumental in keeping its valuation reasonable even as the stock continues to produce excellent gains for shareholders.

Visa is as close to a perfect business model as it gets, making it a quality company to buy in December.

Disney is a well-oiled media machine

On Dec. 4, Disney raised its semi-annual dividend by 33% to $1 per share per year. The stock still yields under 1%, so it's not a viable passive income stream. But the raise embodies the improving strength in the business and why the company is back on track toward growth.

The pandemic took a sledgehammer to its parks and movie business, while the launch of Disney+ in November 2019 ramped up expenses and added to losses since the service was unprofitable until earlier this year.

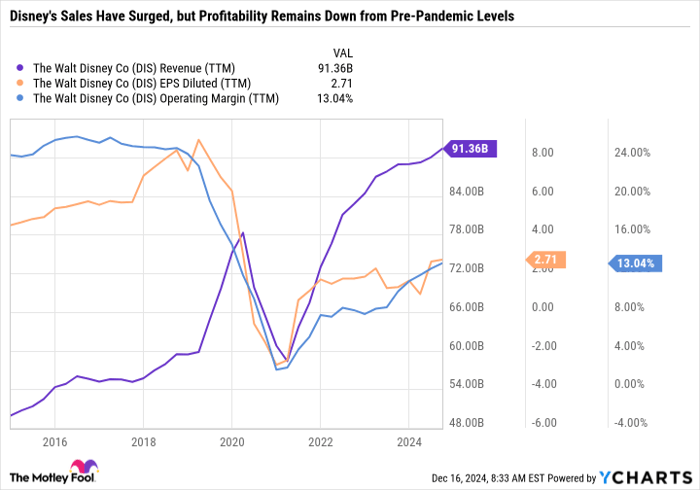

DIS revenue (TTM), data by YCharts.

As you can see in the chart, the company is generating all-time high sales, but its operating margins and diluted EPS are significantly down from pre-pandemic levels.

That's all about to change. Management is guiding for higher earnings growth over the next three years, driven by a consistently profitable streaming segment, blockbuster hits, a strong cruise line and parks business, and more.

Disney was firing on all cylinders pre-pandemic, with smashing hit after hit at the box office, through its Star Wars and Marvel franchises. It has yet to have everything working at once since then, but there are signs the company is heading in the right direction.

What makes it such a compelling buy for December and beyond is that its best days could be ahead. If Disney+ can become a high-margin streaming platform, it will leverage the company's intellectual property like never before.

Pair that with a growing fleet of cruise ships and park expansions backed by a $60 billion budget, and you have what could be a successful transition from a legacy media company heavily dependent on cable networks to a modern entertainment giant built for the digital age.

With a 20.9 forward P/E, Disney stands out as a great value and a stock worth buying now.

Should you invest $1,000 in Microsoft right now?

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $808,966!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Daniel Foelber has positions in Walt Disney. The Motley Fool has positions in and recommends Amazon, Microsoft, Nvidia, Salesforce, Visa, and Walt Disney. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.