New

Up More Than 200% In The Past 5 Years, Can Costco Continue Its Momentum In 2025?

Costco (NASDAQ: COST) is one of the best-performing large-cap retail stocks over the past five years. It continued to show why it's one of the top retailers when it once again reported strong results for its fiscal first quarter. The stock is now up more than 50% on the year and about 235% over the past five years, as of this writing.

Let's take a closer look at the retailer's most recent results to see whether the momentum in the stock can continue.

Another stellar quarter

This was the first quarterly report since Costco implemented a membership fee hike that went into effect in September. The increase was its first membership fee bump in seven years. It took the membership fee from $60 a year to $65 a year, and the Executive Membership fee from $120 a year to $130 a year. Slightly more than half of Costco's members are in the higher tier, in which members get 2% back on most purchases, among other perks.

Membership fee revenue climbed 8% in the quarter to $1.17 billion. However, the company said that, due to the deferred accounting, the membership fee increase only had a minimal effect on its result, accounting for less than 1% of the fee growth in the quarter. Instead, the jump in membership fee income was driven by an increase in members, which rose nearly 8% to 77.4 million paying households.

Its membership renewal rate was 92.8% in North America and 90.4% worldwide. Both numbers were down slightly due to more digital sign-ups, which have slightly lower renewal rates.

Same-store sales, meanwhile, rose 7.1% when adjusting for changes in gasoline prices and foreign exchange. U.S. same-store sales climbed 7.2% (adjusted), while Canadian comparable-store sales rose 6.7% adjusted. Other international same-store sales jumped 7.1% (adjusted). E-commerce revenue increased 13.2% on an adjusted basis.

The strong same-store sales results were driven by increased customer visits, which rose by 5.1% worldwide and 4.9% in the U.S. Excluding gasoline and currency, average transactions were up 2% worldwide and 2.3% in the U.S.

Costco said fresh foods was helping lead the way, with comparable sales up high single digits. It noted meat was particularly strong, up double digits, as it was seeing customer strength at both the high end and lower end of this category. Meanwhile, growth of its Kirkland's Signature brands continues to outpace its business as a whole, while it has been able to lower prices on some items.

Non-food categories were also strong, up high single digits. A number of categories saw double-digit gains, including jewelry, home furnishings, and luggage, among others.

Costco also continues to open new locations. It ended the quarter with 897 warehouse stores. That's up from 871 locations a year ago. It opened seven new clubs in the quarter and expects to open 29 for the year, including three relocations.

Altogether, this led to the company seeing its revenue rise 7.5% to $62.15 billion, with adjusted earnings per share (EPS) climbing 13% to $4.04. That surpassed the analyst consensus looking for EPS of $3.78 on revenue of $62.08 billion.

Image source: Getty Images.

Can Costco's momentum continue?

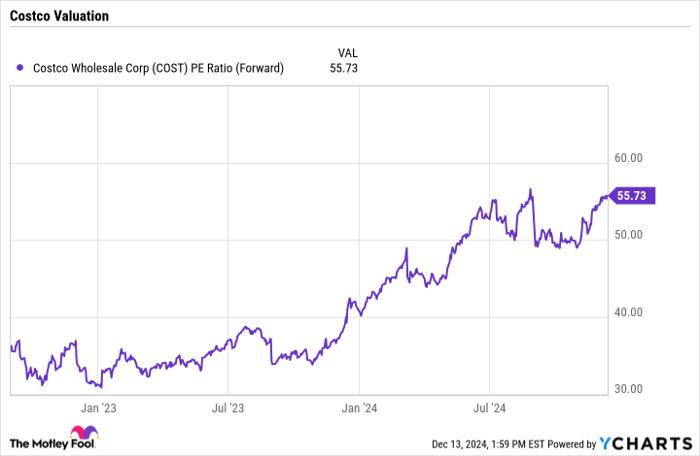

One of the knocks on Costco is its valuation. The stock now trades at a more than 55 times forward price-to-earnings (P/E) ratio. However, questions surrounding Costco's valuation have been a pretty common theme during the past few years, and the stock has nonetheless continued to perform very well.

COST PE Ratio (Forward) data by YCharts.

Meanwhile, with the membership fee increase, the company should see its earnings growth start to accelerate. Its membership fees are essentially 100% gross margin, meaning the incremental revenue growth from the fee increase should drop straight to operating income.

Given its 77.4 million paying members at an average increase of $7.50, and its mix of regular and executive memberships, that equals $580.5 million in incremental operating income, or about $435 million in net income (assuming a 25% tax rate). That would be nearly a $1 boost to its annual dividend given its approximately 443 million shares.

Meanwhile, the company's combination of low prices and convenience continues to resonate with customers, especially as many have struggled from the high-inflation environment in the past few years. As such, I think the stock is likely to just continue chugging along, producing solid investor returns over the long term.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $348,112!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $46,992!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $495,539!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of December 16, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale. The Motley Fool has a disclosure policy.