New

Buying A Home Is Growing Even Less Affordable

With relentlessly high mortgage rates and stubbornly high home prices, the mortgage payment on the median priced home in the U.S. is now back up above the 2023 and 2024 levels for the first time since August. Affordability is getting worse for homebuyers this fall. That does not bode well for home sales in the new year.

We saw two signals that buyers are backing off in the face of mortgage rates. We measured a small acceleration of price cuts, which may have happened when buyers and sellers got disappointed by the cost of money after the election.

Inventory also declined for the week but less than expected. Inventory has been compressing since last year, but it expanded this week. Last year, we were near the top of mortgage rates. This year hasn’t topped out yet. Those two signals are worth watching and we’ve got the details here.

Let’s take a look at the data for the last week of November 2024.

Inventory is moving down

There are now 719,000 single-family homes unsold on the market around the U.S. That’s half a percent fewer than last week. There are just over 27% more homes unsold on the market than last year. That percentage increased from last week. This is a bit of a subtle way to look at the inventory trends, but it implies that the inventory shrinking momentum we’ve had for a few months may have stopped.

When we released the HousingWire 2025 forecast paper earlier this month, we discussed how we assume continued inventory growth in 2025, but at a slower pace of appreciation than we saw this year. We anticipate another 13% inventory growth next year. But we also assume that mortgage rates will moderate a bit. As of right now, mortgage rates are climbing. As rates climb, inventory climbs.

If affordability continues to worsen, that will accelerate inventory build up. The 2025 lines will trend higher, even closer to the old normal levels.

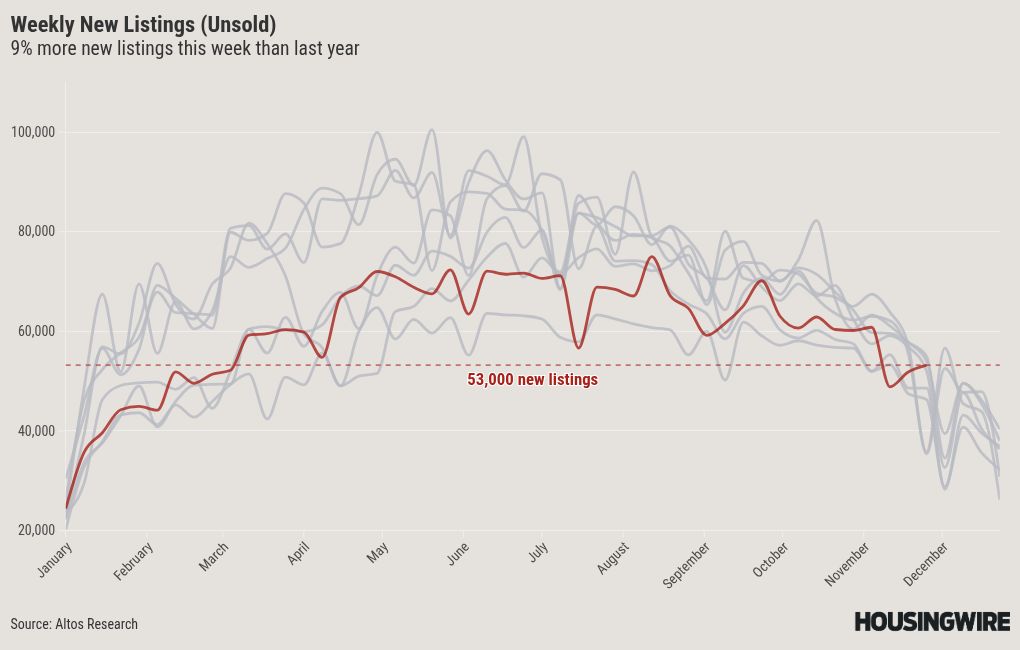

New listings climb

There were 53,000 new listings unsold this week. That’s 9% more unsold new listings than the same week a year ago. This level of new listings will lead to inventory growth. When we add in the 7,800 new listing immediate sales, that’s 4.7% more sellers than a year ago.

In the chart, 5% more sellers than a year ago is right in the range we want to see. The red line is right at the level of pre-pandemic sellers. It’s healthy for the housing market to have slightly more sellers than we’ve had in recent years.

This is the holiday week, so we’ll have a big dip in new listings this coming week.

The takeaway with the new listings data is that we are hopeful. If the market is going to grow in 2025, this data will need to stay with 5-10% more sellers each week than we’ve had in recent years.

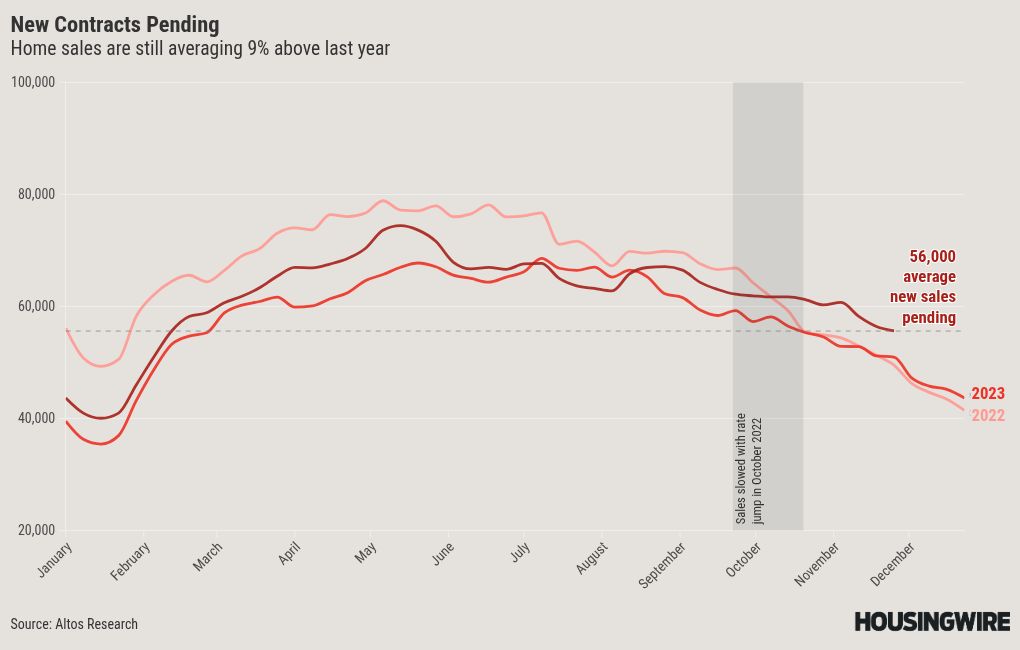

Home sales at average pace

There were 56,000 new contracts pending last week which was a pretty good clip for mid November. That was 6% more new contracts started than a week ago and also 6% more than a year ago.

We’ve been averaging 56,000 new contracts each week for single-family homes. We’re looking here at the average pace of home sales. The homes that start contract now will mostly close in December and January. We recently heard NAR announce October sales grew over last year. We can see that in the Altos data each week.

The takeaway on home sales is that we’re counting slightly more home sale transactions than last year — finally. I expect that growth to continue into 2025, but it’s not a lot of growth. We’re forecasting 4.2 million home sales in 2025 up from 4 million in 2024. We’ll see that trend in this chart each week. If the trend falls, we’ll review our forecast lower. Stay tuned.

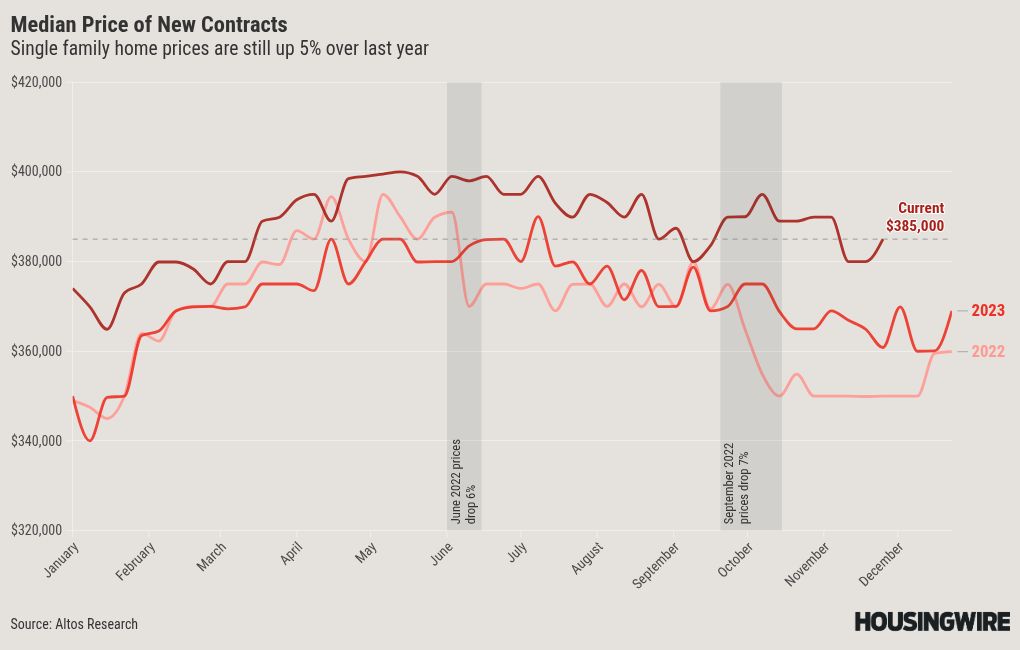

Home prices tick up

Despite the affordability crisis, we measured an uptick in the price point for home purchases this week. The median price of the newly pending home sales was $385,000, which is a 1.3% increase from a week ago and is averaging 5% more than last year. Even with 7% mortgage rates and the highest mortgage payment ever, home prices nationally have not dipped.

Home prices are holding up better than expected with demand that was weak earlier this year. We measure the sales prices — before the sale happens. This is the price point people are buying. Asking prices are up over last year, too. The median price of all the homes this week is $429,900, which is 1% above last year.

The median price of the new listings for the week came in at $397,000. The price of the new listings has been averaging about 3% above last year.

It’s hard to imagine scenarios next year where home prices rise dramatically unless there is some crisis which lowers mortgage rates into the low 5s. In the HousingWire forecast paper, we published several scenarios where home prices could fall nationally in 2025. We examine these scenarios and identify data that you can watch to know if one of these home price correction scenarios is underway. Affordability is a legitimate reason to assume home prices could fall next year.

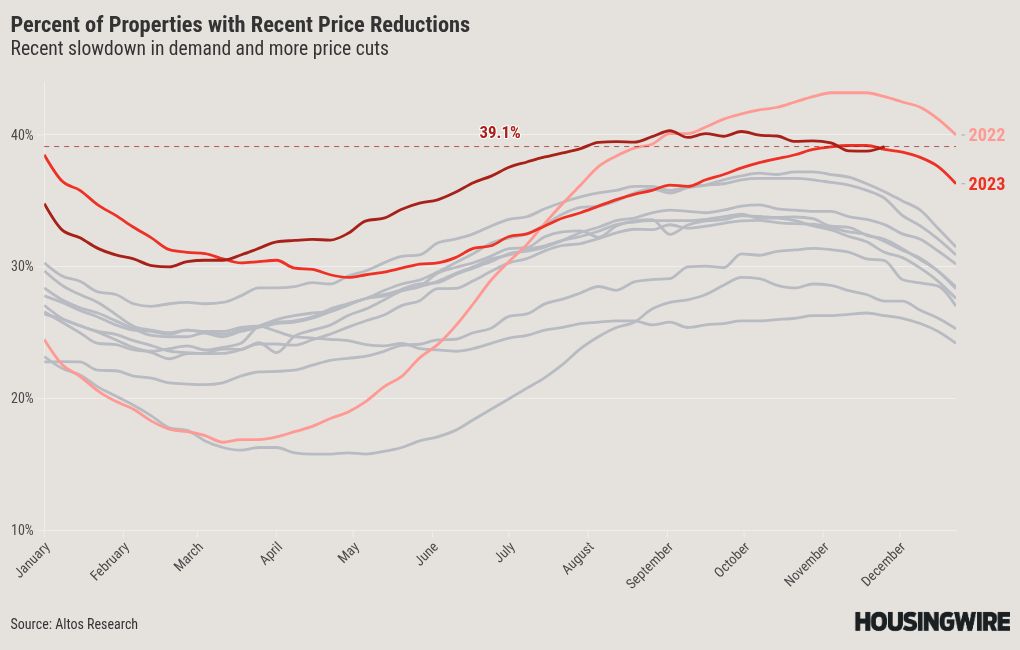

Price reductions tick up

Some of the data looks into the future for price trends, and when we look there, we can see a signal that prices are softening with these recently elevated mortgage rates. The percent of homes on the market with price reductions ticked up this week to 39.1%. It seems likely that there are some sellers who didn’t quite get the deal done in October. Now, after the election, mortgage rates have risen again, so those homes didn’t get offers.

If your house is listed and the market cooled after the election, you have two options, you can withdraw to try again in the spring, or you can cut your asking price. It looks like some are cutting their asking prices.

In each of the last two years, late November was the peak of mortgage rates and the peak of price reductions. It’s the holidays, so homes that haven’t had offers will commonly be withdrawn from listing so they can try again after the new year.

In the Altos data, we look back over 90 days to measure price cuts. Most MLSs let you withdraw for 30 days and relist as a new listing. Altos tracks those relists. If a house is pulled at Thanksgiving, and relists in January at a lower price, we’ll see that in January and track it as a price reduction.

Mike Simonsen is the founder of Altos Research.