New

Distressed Properties Signal A Slowdown In 2025 Housing Market

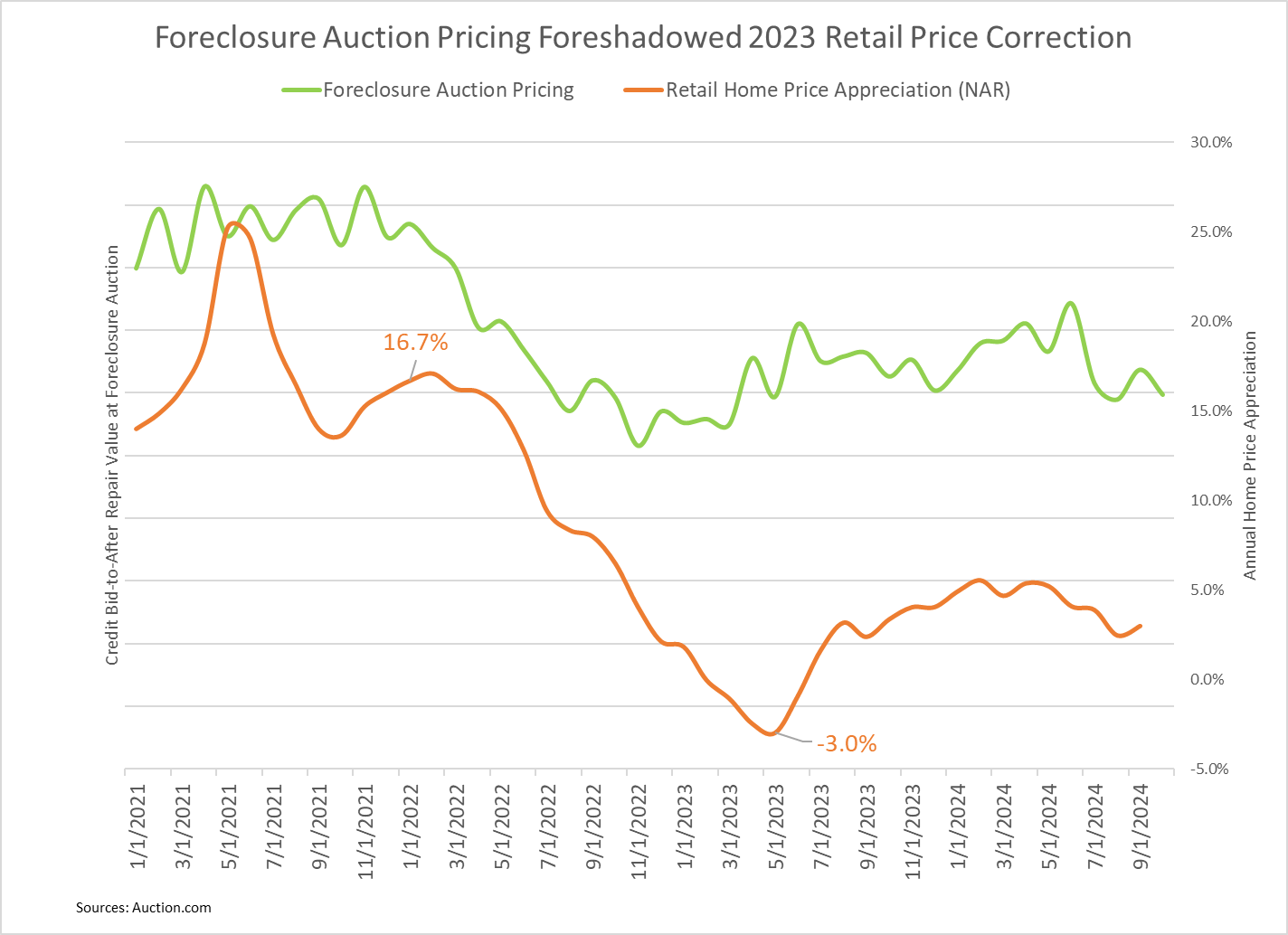

Institutional sellers at distressed property auctions have gradually lowered pricing over the last six months as rising retail inventory and stubbornly high mortgage rates act as twin headwinds for buyers purchasing at these auctions. This downward pricing trend at distressed property auctions, combined with affordability constraints for retail buyers and rising rates of serious delinquency, foreshadows slowing home-price appreciation in 2025.

Proprietary data from the Auction.com marketplace, which accounts for close to half of all properties brought to foreclosure auction nationwide, shows that banks, nonbanks and mortgage servicers selling on the Auction.com platform have slowly lowered their pricing at both foreclosure auctions and bank-owned (REO) auctions over the past six months.

How auction pricing works

Pricing in the auction context is best measured over time by the reserve set by the seller relative to the estimated after-repair value of the property being sold. The reserve, known as reservation price in auction theory, is simply the minimum amount a seller is willing to take to sell. The after-repair value is the estimated full market value of a property in fully repaired condition. By definition, most distressed properties sold at auction are in need of substantial renovations.

One additional twist is that the reserve at foreclosure auction — also know as the credit bid — is often capped by statute at the total debt owed to the foreclosing lender. In some cases, this capped credit bid is lower than the market-driven reserve price. This is not the case for REO auctions, in which the seller is free of restrictions in setting the reserve and typically does so based on some variation of a net present value (NPV) analysis.

Register today to attend the Housing Economic Summit in Dallas, on Feb. 26, 2025 and hear Daren Blomquist in person. The summit is designed to give you a comprehensive understanding of the economic factors driving the housing market in 2025 — and what it all means for your business.

Auction pricing reduction

The Auction.com data shows the average reserve-to-value ratio at REO auctions dropped by 2 percentage points in the six months ending in October while the credit bid-to-value ratio at foreclosure auction dropped by 3 percentage points in the four months ending in October.

These drops are noteworthy given the narrow range that the reserve-to-value ratios typically operate in and given that similar previous drops in the ratios have foreshadowed a slowdown in retail home price appreciation — even to the point of home price appreciation turning negative for five consecutive months in the first half of 2023, according to data from the National Association of Realtors (NAR).

The five-month run of negative retail home price appreciation — which started in February 2023 — was preceded by a 7-point drop in the average credit bid-to-value ratio at foreclosure auctions between January and November of 2022 and by a 6-point drop in the average reserve-to-value ratio at REO auctions between July 2022 and February 2023.

Auctions as a leading indicator

Why do bidding and pricing trends at distressed property auctions often act as a leading indicator for retail housing market trends?

First, distressed property buyers have their finger on the pulse of their local housing market, pulling from the anecdotal data and hard data that comes from a high velocity of transactions. Furthermore, these distressed buyers are often local community developers whose success depends on accurately predicting the retail market in the three to six months it takes them to renovate a property.

Second, institutional distressed property sellers typically respond more quickly than retail sellers to market conditions because they are not emotionally tied to the properties they are selling. Listening and responding to the market helps them sell faster, reduce holding costs and optimize their net proceeds from a sale.

More pressure on prices

But it’s more than just lower pricing at distressed property auctions that point to slowing home price appreciation in 2025. The broader trends of rising retail inventory, stubbornly high mortgage rates and inflated price-to-income ratios are all continuing to put downward pressure on home prices. Meanwhile, seriously delinquent mortgage rates just recently turned a corner higher after a three-year downward trend, another headwind for home prices.

Active inventory of homes for sale in October 2024 increased 29% from a year ago to 953,814 — the highest level since December 2019, according to an Auction.com analysis of data from Realtor.com. The annual inventory increases were much higher in some markets, including Miami (up 57%), Atlanta (up 47%), Denver (up 59%), Las Vegas (up 49%), and Seattle (up 60%).

Mortgage rates have remained stubbornly high, hovering around 7% despite the Federal Reserve’s September rate cut. Recent comments from Fed chairman Jerome Powell indicate that more rate cuts may not be coming as fast as previously anticipated.

“The economy is not sending any signals that we need to be in a hurry to lower rates,” he said at a recent event in Dallas.

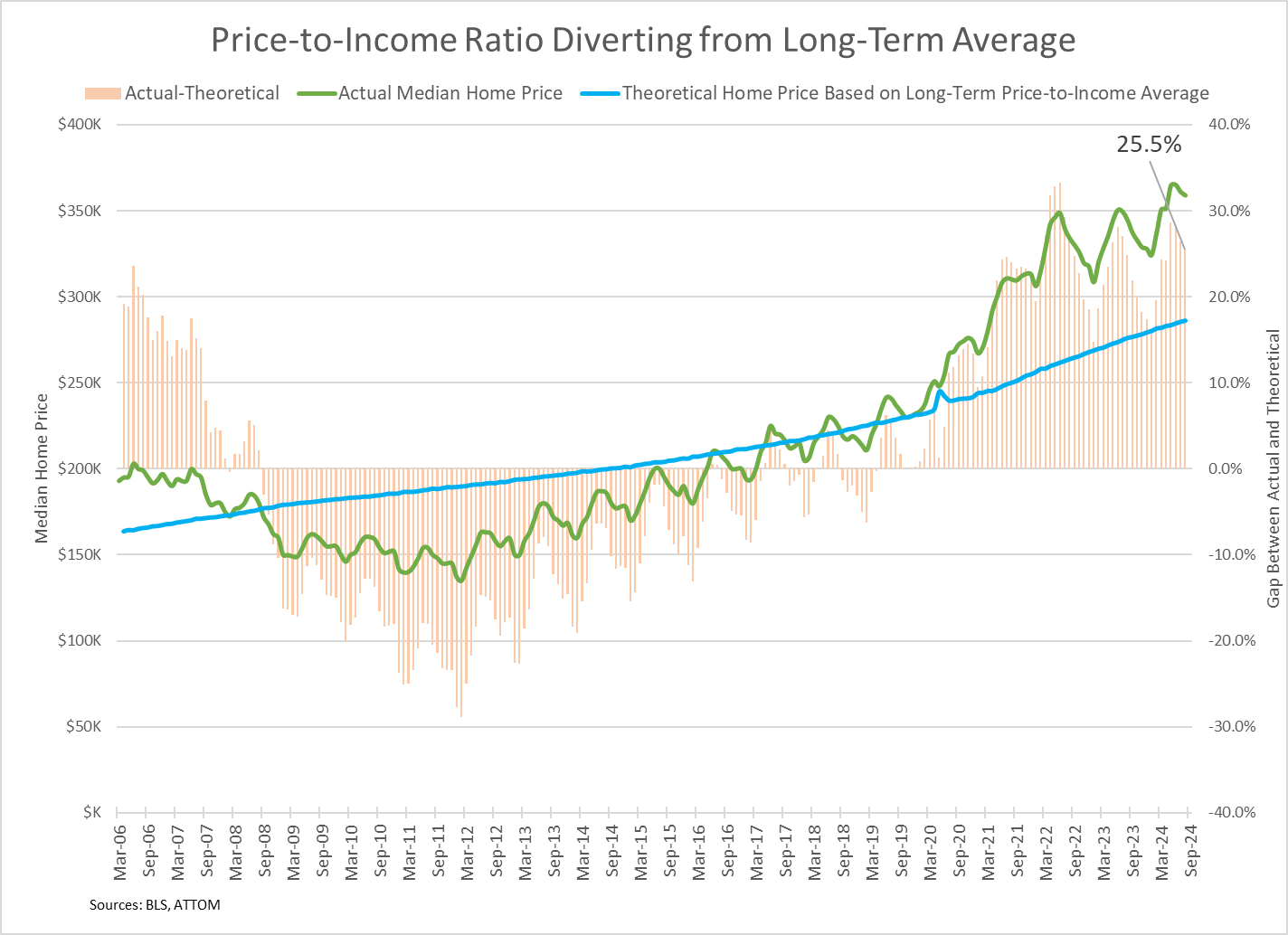

National price-to-income ratios continue to run at about 25% above their historical average, according to an Auction.com analysis of median home price data from ATTOM Data Solutions and average weekly wage data from the Bureau of Labor Statistics. Returning to that historical average would require some combination of decelerating home price appreciation and accelerating wage growth.