New

Housingwire’s Mortgage Rate Forecast For 2025

I like to say that I don’t predict mortgage rates — and I’m not convinced that anyone can. Bond markets are driven by so many unpredictable factors that even the wisest market visionaries have big blind spots. Look no further than a year ago when the prospect of recession in the U.S. seemed inevitable and mortgage rates were commonly expected to fall into the 5s for most of 2024. None of that happened. Predicting mortgage rates is hard.

That being said, we do have some insight about what is likely to happen with mortgage rates over the next year. And since mortgage rates drive so much of the U.S. housing market, I thought I’d collect the best thinking here. We recently released the HousingWire Housing Market 2025 Forecast. In it we discuss our expectations for home sales and home prices in the next year and the mortgage rate assumptions that drive the forecast. These are the assumptions from that research.

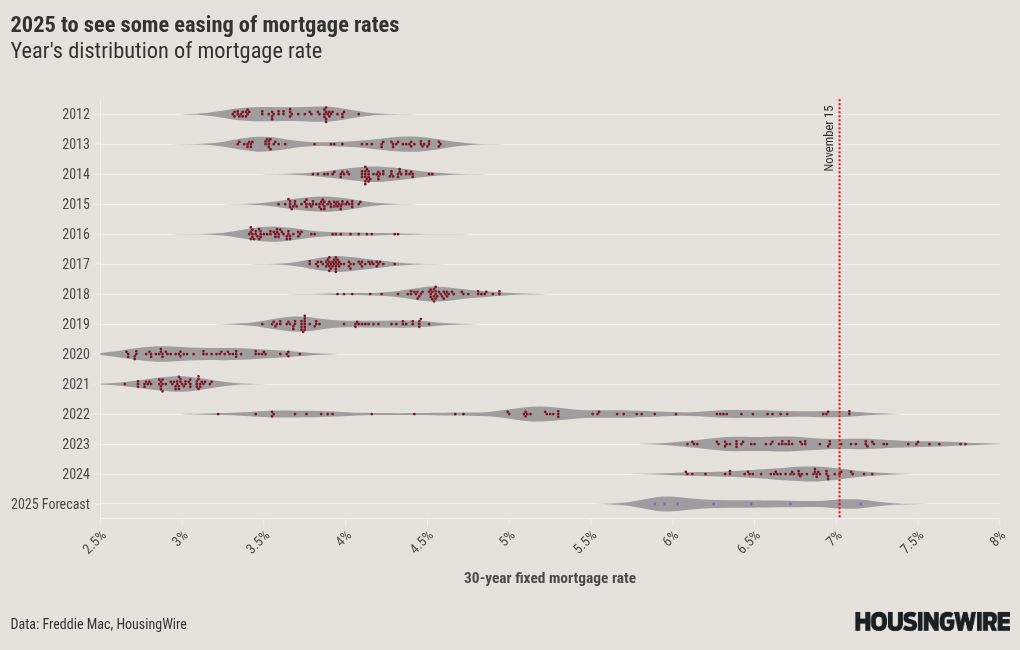

The interest rate for the 30-year fixed rate mortgage has stayed higher for longer than anyone anticipated three years ago. At the start of 2024, expectations were generally that mortgage rates would fall during the year. But in fact, rates spent most of the year closer to 7%, with peaks in May and again in November, where we are now.

The HousingWire Mortgage Rate Forecast for 2025

HousingWire expects the 30-year fixed rate mortgage to spend the bulk of the 2025 calendar year in a range from 5.75% – 7.25%.

A range of 150 basis points in a year is pretty broad, but in the last three years mortgage rates moved in 140bp range (2024), 200 bp range (2023) and a whopping 400bp range in 2022. See the chart below for the distribution of mortgage rates over the last 13 years. In light of recent market trends, a 150 basis point range in 2025 seems plausible. When rates were low, the range was much smaller.

HousingWire’s lead analyst, Logan Mohtashami, highlights several macroeconomic variables that contribute to the range for mortgage rates in the coming year: economic growth, inflation, unemployment and the possibility of outright recession.

One big miss for forecasters in 2024 was that many assumed a recession was imminent. The headlines and the conventional wisdom saw a recession around the corner starting in late 2021 and by late 2023, many were certain recession was upon us. But the U.S. economy defied expectations and kept growing. As a result, mortgage rates stayed surprisingly elevated as well.

Contrary to the impact of recession expectations on interest rates is the power of inflation. In 2024, the prospect of inflation forced the Federal Reserve to keep short-term interest rates higher for longer. Finally in September, the Fed started its easing cycle. About that same time, the markets began anticipating a Trump victory and broadly speaking, the market views Trump’s economic plans as inflationary. As a result, yields on the 10-year treasury began rising even as the Fed started cutting.

Logan likes to point out that the Fed is still not “accommodative,” meaning that the Fed is more focused on restraining inflation than cutting rates to encourage economic growth and accelerate hiring. The Fed’s “pivot” from restrictive to accommodative hasn’t yet happened.

HousingWire’s Flavian Nunes points out how sensitive, even if indirectly, mortgage rates have been to Federal Reserve policy.

The 10-year and the spread

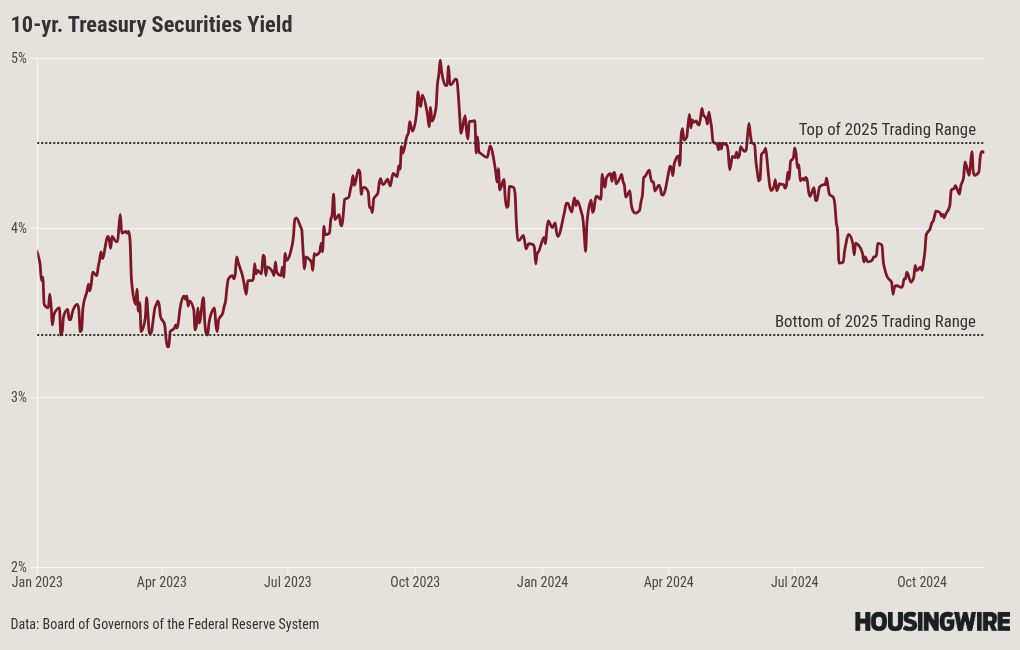

Mortgage rates are loosely tied to the yield of the 10-year Treasury. For 2025, we expect the yield range to be between 3.4% and 4.50% for the 10-year. Logan points out that absent any economic data indicating recession is upon us, the 10-year yield probably won’t go lower than 3.40%. If the economy continues to outperform expectations, the yield could push above 4.5%.

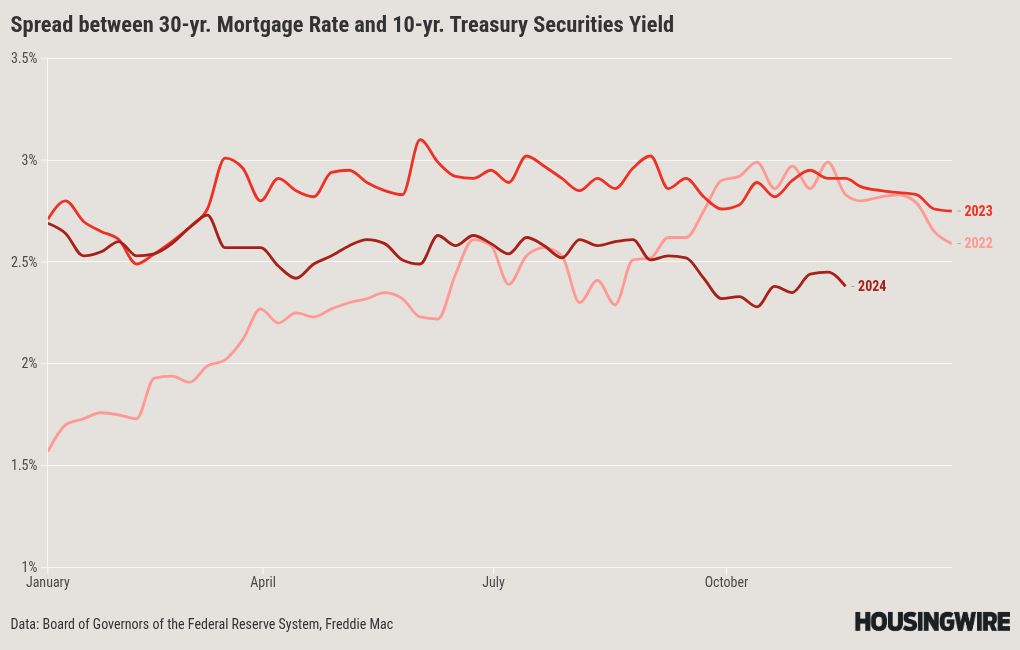

Mortgage rates trade at a premium to the yield on 10-year Treasury. The premium is known as “the spread.” As interest rates fell to record lows during the pandemic, the spread also fell to record lows. As rates spiked dramatically in 2022, that volatility forced investors to require a greater interest rate on mortgage securities and the spread increased. In the past three years, the underlying interest rate increased and the spread increased as well. Mortgage rates paid by the homebuyer got hit with a double whammy.

As interest rates have stabilized, the spread in 2024 has eased lower, from 291 basis points a year ago, to 238 basis points today. We expect stability on the underlying bond markets to allow mortgage spreads to continue to ease a bit lower in 2025. If during the year, the 10-year yield falls to the low end of the expected range, say 3.5%, and the spread eases down to 225 basis points, those moments would indicate mortgages available for 5.75%.

A slowly decreasing spread gives us a little optimism that mortgage rates will touch the low end of the range in our forecast for the year.

Unfortunately for homebuyers in the U.S. housing market, it seems unlikely that the growing U.S. economy, the bond market and the spreads will conspire to create a scenario where mortgage rates fall far enough to alleviate the affordability challenges faced by so many in the last three years.

Read the whole HousingWire Housing Market 2025 Forecast.