New

How Are Mortgage Rates Affecting Housing Demand?

It has been almost two months since mortgage rates spiked again, and my initial thought was this would tank housing demand. We had a positive 18-week period with purchase applications before mortgage rates started rising in September. I figured those increases would produce the same weakness in purchase apps that we saw earlier in the year. However, surprisingly, demand has held up better than I anticipated. We aren’t growing like before, but we aren’t as negative as I thought either. Let’s take a look at the data.

Purchase application data

We have had six weeks of rising mortgage rates and I had anticipated purchase apps to be primarily negative. Instead, we are flat, with three positive and three negative purchase application data prints on the week-to-week data.

When mortgage rates were running higher earlier in the year (between 6.75%-7.50%), this is what the purchase application data looked like:

- 14 negative prints

- 2 flat prints

- 2 positive prints

When mortgage rates started falling in mid-June, here’s how purchase applications responded:

- 12 positive prints

- 5 negative prints

- 1 flat print

I expected more weakness as rates rose. I am curious about the next few weeks because, in the last two years, we had an early spring run in demand with application data, but that was with rates falling. Last week saw 2% week-to-week growth but was down 1% year over year.

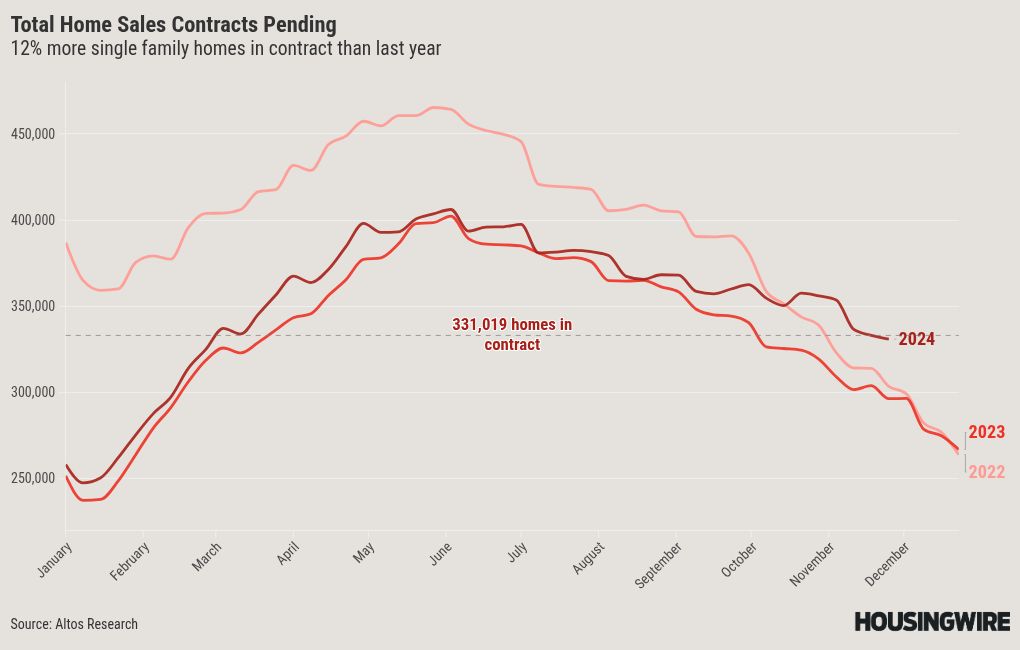

Weekly pending sales

The Altos Research weekly pending contract data provides insights into real-time demand. This data tends to be seasonal, as illustrated in the chart below. Initially, the data showed more robust performance as mortgage rates approached 6%. Even today, the pending contract data remains resilient despite higher home prices and mortgage rates than last year. This has caught my attention and is something I am following closely.

The next time mortgage rates head toward 6%, assume that the demand curve gets better. But let’s be honest here: we are working from depressed sales levels.

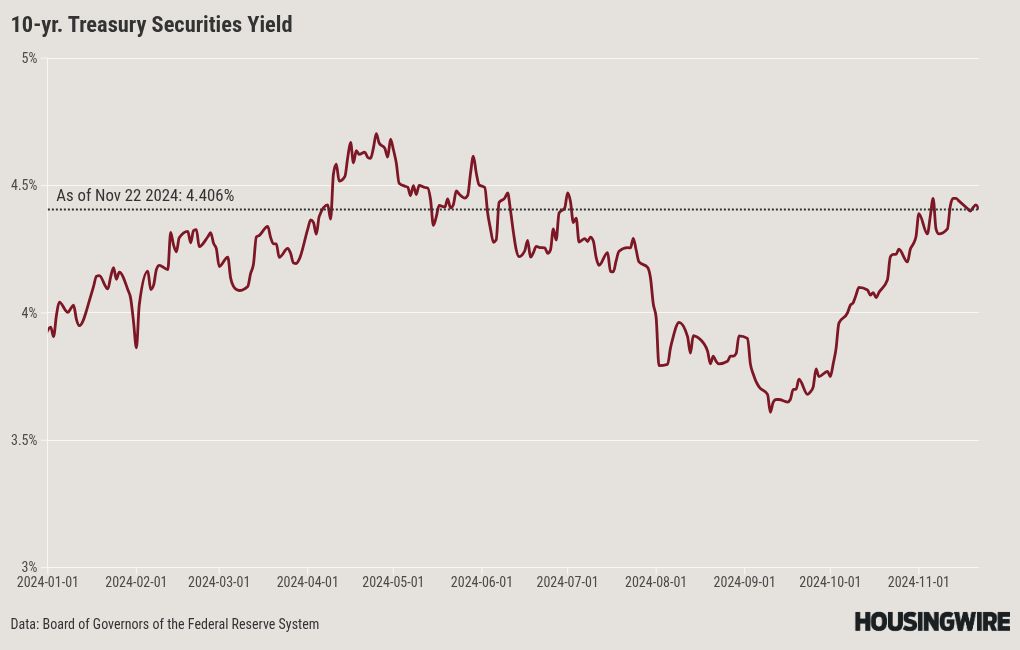

10-year yield and mortgage rates

My 2024 forecast included:

- A range for mortgage rates between 7.25%-5.75%

- A range for the 10-year yield between 4.25%-3.21%

This week was relatively calm for mortgage rates as the 10-year yield continues to hold steady at a critical level, which ranges from 4.40% to 4.50%. Given the inflation data and statements from the Federal Reserve, the past two weeks could have been interpreted as hawkish. However, the 10-year yield has managed to maintain its position, and the downtrend observed in the charts since the 10-year yield was at 5% in 2023 is still in place. Additionally, I’ve noticed that the Citigroup Economic Surprise Index, which usually fluctuates in tandem with the 10-year yield, is also peaking in the short term.

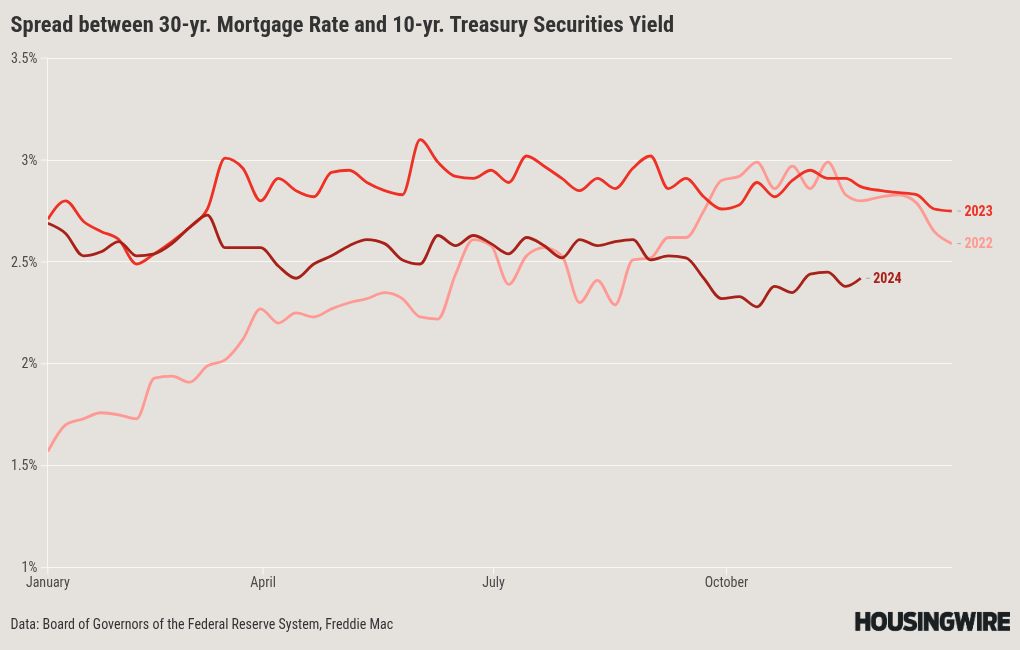

Mortgage spreads

The mortgage spread situation has shown improvement in 2024, in contrast to its negative performance in 2023. With these spreads improving, mortgage rates have been able to approach 6% at different times this year. Without this spread improvement, mortgage rates would currently be over 7.50%.

Spreads have worsened slightly since mortgage rates started rising in September, but they remain far better than the disastrous peak levels experienced in 2023. If the spreads were as high as they were then, mortgage rates would be 0.68% higher today. Conversely, if we had average spreads, mortgage rates would be lower by approximately 0.75% to 0.85% today.

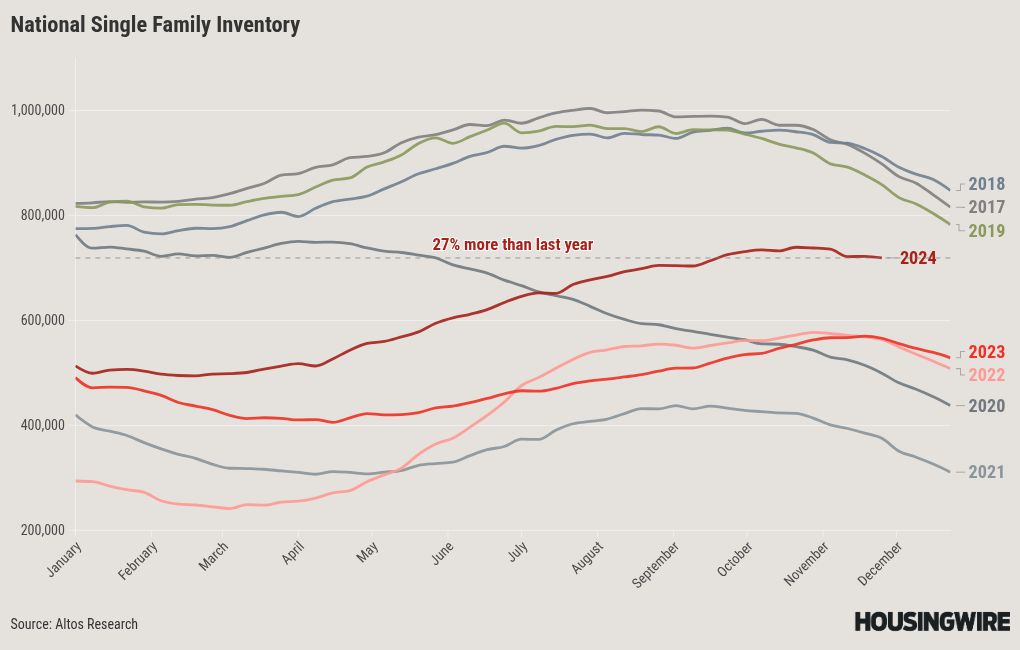

Weekly housing inventory data

Last week saw another slight decline in active listing and soon, the holidays will kick in. I thought we might see a small pop in supply before Thanksgiving week, but no. The seasonal decline is well underway, and it looks like the 739,434 level will be the peak of inventory for 2024.

- Weekly inventory change (Nov. 15-Nov. 22): Inventory fell from 722,032 to 719,055

- The same week last year (Nov. 17-Nov. 24): Inventory fell from 569,898 to 565,875

- The all-time inventory bottom was in 2022 at 240,497

- The inventory peak for 2024 so far is 739,434

- For some context, active listings for this week in 2015 were 1,104,310

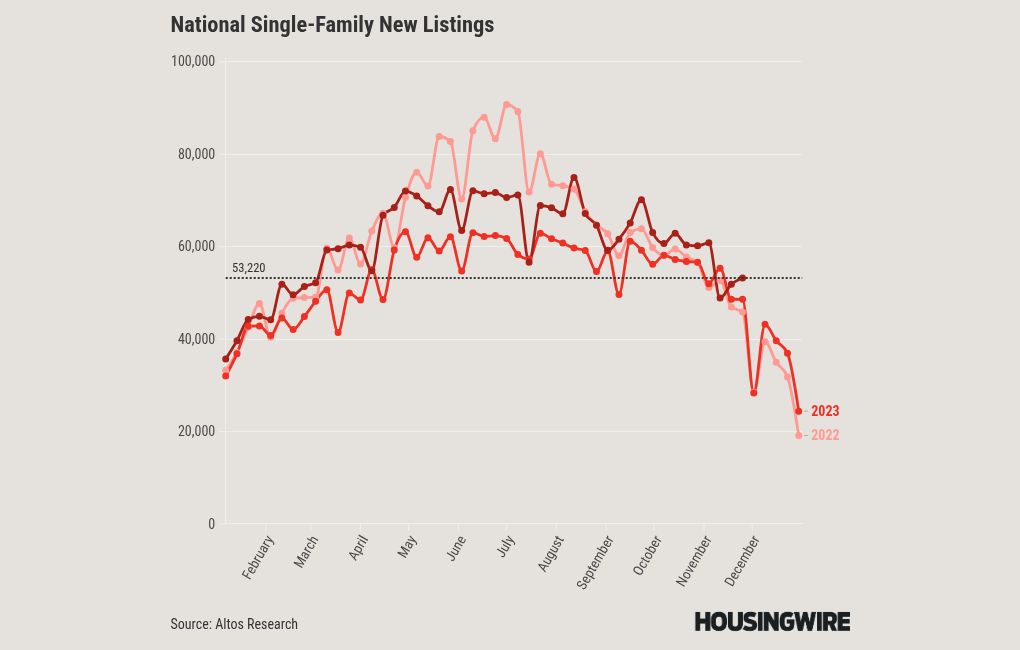

New listings data

While active inventory didn’t rise, we did get a nice boost in new listings this last week. Still, when it’s all said and done, 2024 will be the second-lowest new listings year in history. We haven’t seen stress sellers on any scale that all those terrible YouTube accounts have been pushing for years.

The goal for 2025 is to get new listings back to normal, which means that during the seasonal peak period, we should get new listings between 80,000 and 110,000 per week. During the housing bubble crash years, this data line was running between 250,000-400,000 per week for years. Here are the number of new listings for last week over the last several years:

- 2024: 53,220

- 2023: 48,587

- 2022: 45,859

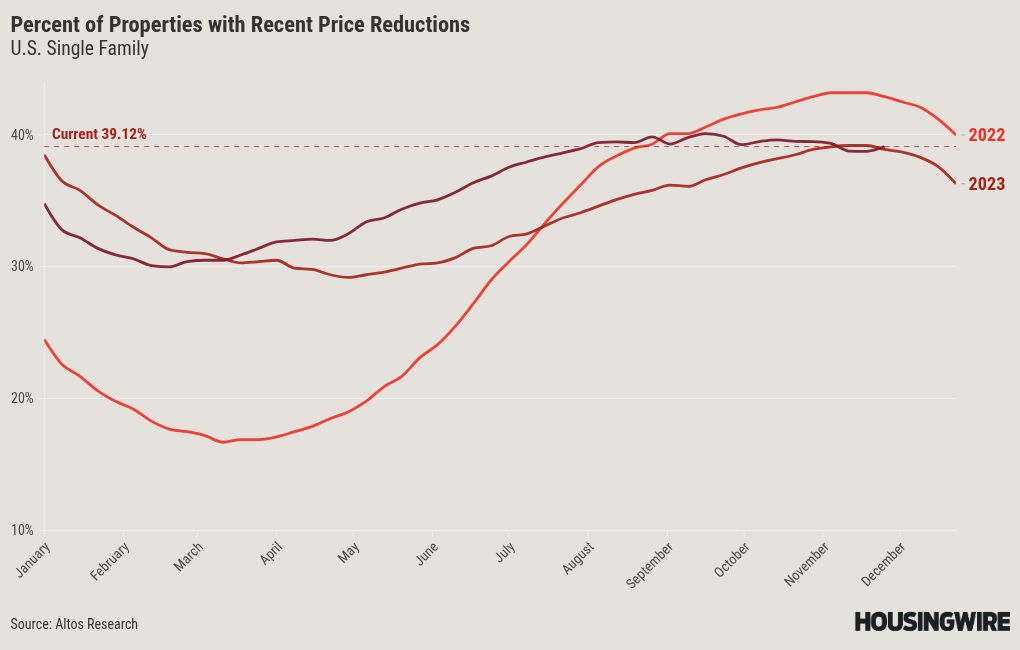

Price-cut percentage

In an average year, one-third of all homes experience a price cut, which is typical in the housing market. When mortgage rates increase, the percentage of homes reducing prices tends to rise. Conversely, this trend can slow down when rates decrease and demand increases, as recently when rates fell. However, rates are back higher again. As we can see, we are at the same levels today as we were last year, even with more inventory.

Here are the price-cut percentages for last week compared to previous years:

- 2024: 39.1%

- 2023: 39%

- 2022: 43%

The week ahead: Home prices, new home sales, bond auction and inflation data

This week is a holiday week, which means all hands aren’t at the trading desk, so we can see some volatility in markets, especially with some bond auctions happening. The markets will normalize after Thanksgiving, so it’s important to view the movements of the 10-year yield with some skepticism as mortgage rates might fluctuate a little bit more than normal this week.The new home sales data will be particularly significant as that reflects the economic cycle and recent purchase application data for builders has been positive.

We also have the Fed’s PCE inflation data this week, which will be a factor for the next Federal Reserve meeting, although labor data is more critical. Home-price data is expected to show a cooling trend in growth compared to the highs earlier in the year. Additionally, keep in mind that jobless claims data can be unpredictable around holidays, so it’s important to consider this over the next few weeks.