New

Today’s Sellers Don’t Have To Worry About Underwater Mortgages

The recent CoreLogic Homeowner Equity Insights report for Q3 shows a continued positive trend of a lack of underwater mortgages in America today. Underwater mortgages — where borrowers owe more on their home than what it is worth — pose a risk of foreclosure and hinder people from selling their homes, something that was rampant after 2008.

In 2010, more than 23% of homes in America were underwater. Our new listing data for that time period shows there were between 250,000 and 400,000 new listings per week as many sellers with underwater mortgages were forced into a distressed market. This resulted in a higher level of distressed sales compared to historical averages.

However, the housing credit market has improved dramatically since then, empowering homeowners looking to sell and buy their next house. Underwater mortgages are a proper barrier for sellers — more so even than mortgage rates. Therefore, the fact that this data line is just 0.1% away from all-time lows makes me smile this holiday season.

Currently, only approximately 1.8% of homes are underwater, which equals around 990,000 homes. The chart below illustrates that there are few underwater homes today, while many homeowners have significant equity. Additionally, this data doesn’t even include the 40% of homes in America that are mortgage-free.

The chart below shows which states experienced gains or losses in equity year-over-year. This information provides valuable insight into where equity growth occurred.

According to a recent survey by the National Association of Realtors (NAR), the median down payment recently for all buyers is 18%, compared to down payments in the single digits during the housing bubble crash period. This puts recent homeowners in a strong position, providing them with a reasonable cushion should the economy face any severe downturns.

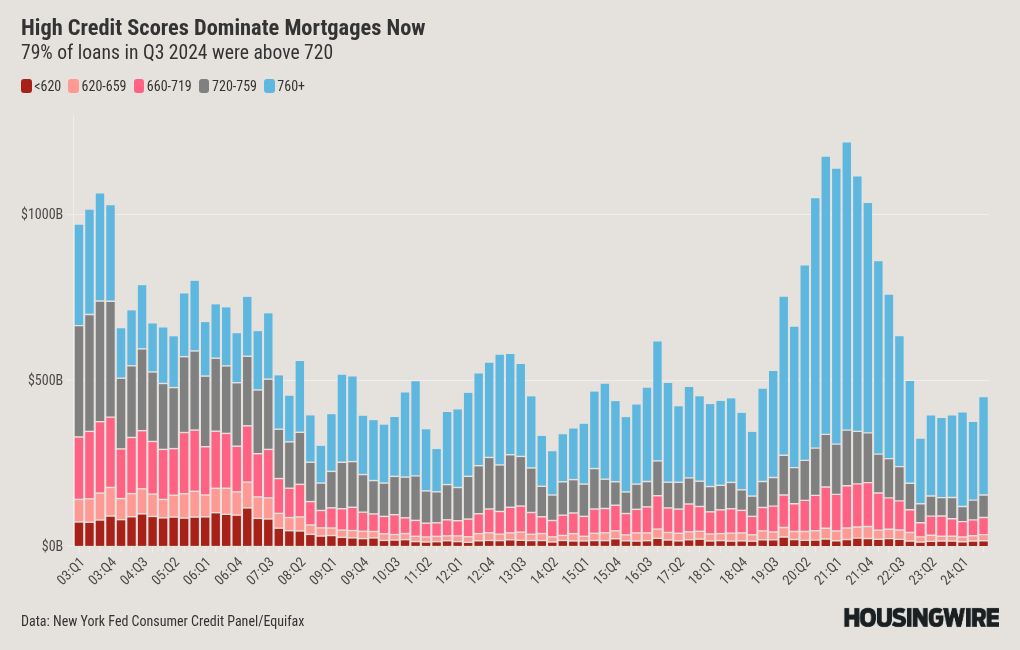

And this kind of downpayment gives them a good starting point for when they do sell and buy their next home. Let’s remember how stellar the U.S. homeowner FICO score data looks this time around; the capacity of sellers being able to turn around and buy is much better now.

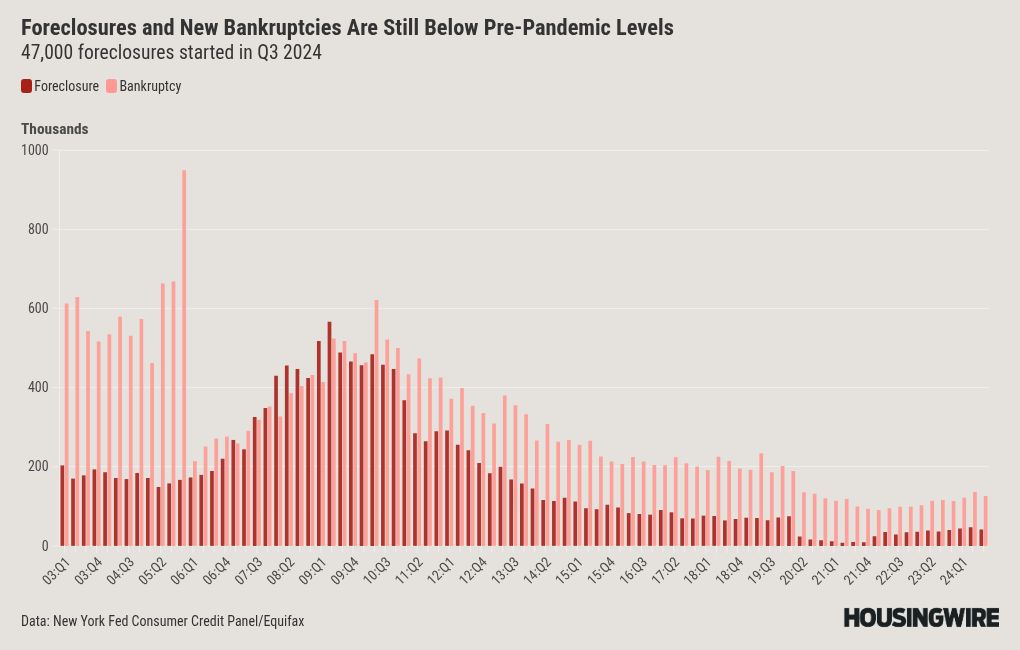

The moral of this story is that we are not at risk for a foreclosure crisis like we experienced during the Great Financial Recession, as we saw massive credit stress build up years before the 2008 recession occurred. Also, homeowners have plenty of equity if they want to sell for whatever reason.

During the recovery from the housing bubble crash, many homeowners who wanted to sell had to either wait or pay cash to cover the difference of what they owed. Now, since there are very few homeowners who are underwater, once mortgage rates decrease, they will have enough equity to sell their homes and purchase another one.

In addition, since Freddie Mac and Fannie Mae are in conservatorship, we don’t need to be concerned about tighter credit in a market where many homeowners are underwater. Unlike in 2008, we will likely experience fewer foreclosures during the next recession when it happens. Additionally, more homeowners can sell their homes and purchase new ones. This is something to feel optimistic about as we approach the holiday season!